“No transfer fee” almost never means no cost The real cost of sending money abroad — the exchange-rate margin, correspondent fees, and cheaper rails.

Somewhere on the transfer page you’ll see it: “$0 fee,” “no transfer charge,” “send money free.” It’s a real feature, and it isn’t the whole price. Every way of moving money across a border carries two costs stacked on top of each other: the fee you can see, and the exchange-rate margin folded into the conversion, which almost never shows up as a line item. The margin is usually the bigger of the two, which is exactly why a “free” transfer can cost more than one that openly charges a few dollars. This guide walks through both costs, how a SWIFT bank wire can arrive short of what was sent, where stablecoins genuinely help and where they don’t, and how to compare routes on the one number that actually matters: what lands in the recipient’s account. It is general education, not financial advice, and every figure below is illustrative, not a live quote.

On this page

- The fee you see and the margin you don’t

- How the margin works, and how to see it

- SWIFT wires, correspondent banks, and why the recipient can get less

- Compare the amount received, not the headline fee

- Bank wire, transfer specialists, cash pickup, and card networks

- Stablecoins as a cheaper rail — and the real trade-offs

- Habits that quietly cost more

- Questions people ask

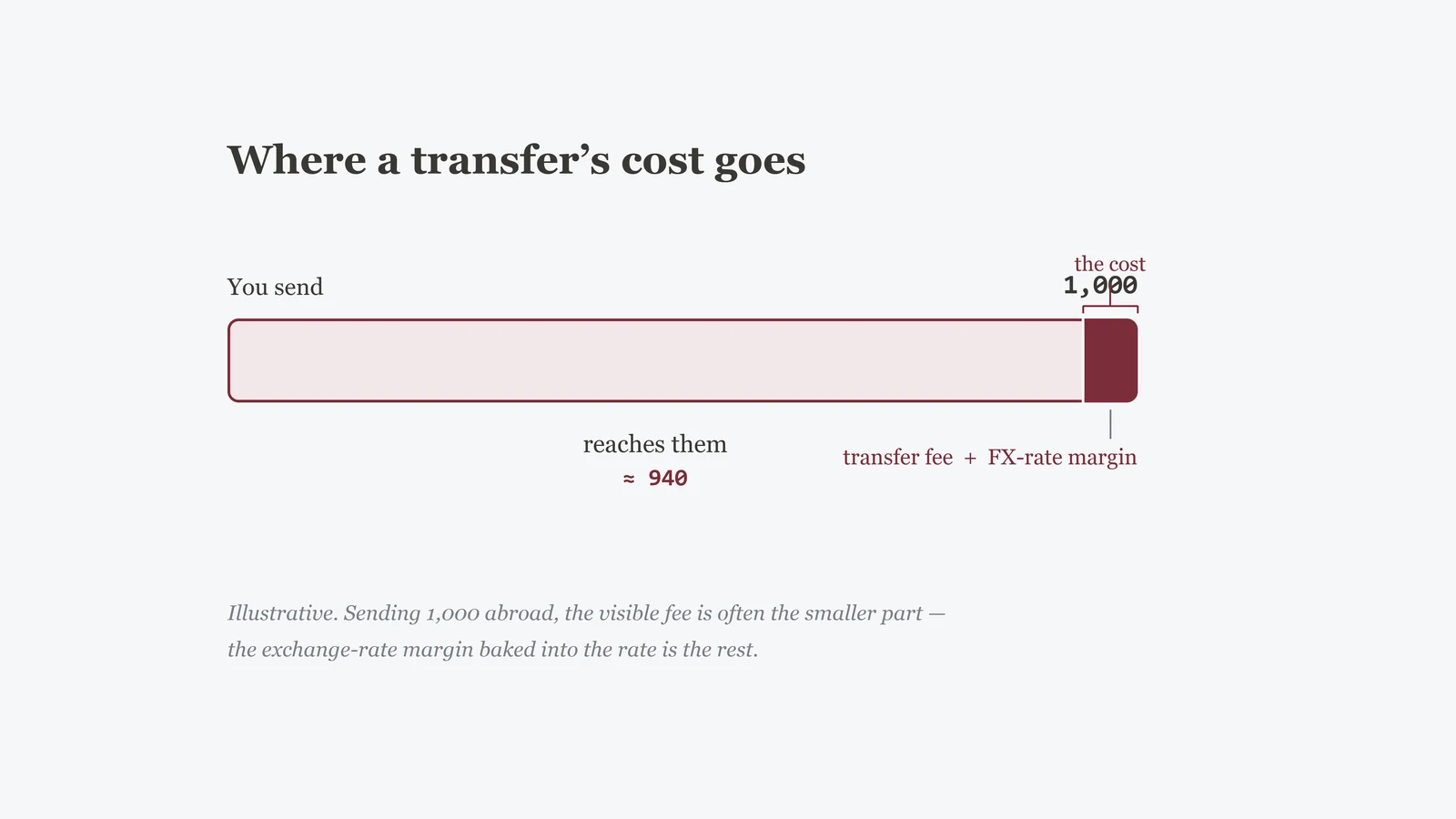

The fee you see and the margin you don’t

Every transfer that crosses a border carries two separate costs, and typically only one of them is advertised. The first is the transfer fee: a flat charge or a percentage, shown on the page before you send. The second is the exchange-rate margin: the gap between the rate you’re offered and the real mid-market rate, the wholesale benchmark banks trade at among themselves. A provider that quotes a rate a little worse than the mid pockets that difference, and nothing on the confirmation screen calls it a fee.

Research into the actual cost of remittances backs this up. The World Bank’s Remittance Prices Worldwide database, which tracks fees and rates across hundreds of country corridors, put the global average total cost of sending $200 at 6.36% in the third quarter of 2025, down from 7.42% in 2016, but still more than double the United Nations’ target of under 3% by 2030 under Sustainable Development Goal 10.c. Banks were the most expensive provider type in that same data, averaging close to 15%, while digital-only services averaged under 4%. Almost none of that gap comes from a bigger sticker-price fee; nearly all of it comes from the rate.

Separate pricing research generally puts a bank’s exchange-rate margin somewhere between 1% and 3.5% above the interbank rate, and it’s common for that margin alone to run past 2% on an ordinary retail transfer, often several times the size of the flat fee sitting right next to it on the same page. On a $1,000 transfer, a 2% margin is $20 gone before any fee is added; a $5 flat charge, by comparison, barely registers. The two costs don’t scale the same way, which is exactly why adding them in your head gets the wrong answer, and why a percentage-based measure is the only fair comparison.

- The fee is the easy part. It’s printed, it’s a fixed number, and it’s the one thing every provider is happy to advertise, including as zero.

- The margin is the real number. It never appears as a line item; it lives inside the rate itself, and on most transfers it’s the larger of the two costs.

- Percentage costs scale with the amount; flat fees don’t. A margin that looks trivial on $50 becomes real money on $5,000, and the crossover between “cheap” and “expensive” moves with the amount you’re sending.

- “Fee-free” describes one ingredient, not the total. Judge the whole cost by what lands in the recipient’s account, not by whether the fee line reads zero.

How the margin works, and how to see it

The mechanism is simple once you know to look for it. A provider sets its own exchange rate a little worse than the honest mid-market rate, converts your money at that internal rate, and the difference is its profit, collected automatically, with no separate charge to point at. Nobody sends you a receipt for the margin; it’s just baked into a number you never see: the rate you would have gotten if the conversion were priced at the true mid.

You can still measure it. Take the exact amount your recipient will receive (or did receive), and work out what exchange rate that implies against the amount you sent. Compare that implied rate with the real mid-market rate for the same pair at the same moment, and the percentage gap between them is the margin: the whole hidden cost, in one number. The full step-by-step arithmetic, with a worked example, is laid out in the mid-market rate and the margin; if you’d rather not do it by hand, the exchange-rate margin calculator does the reversal for you.

This is worth doing before you commit, not after. Ask for the exact amount that will land in the recipient’s account or wallet before you send; a provider that won’t show you that number in advance is telling you something. Once you have it, the margin stops being invisible; it’s just arithmetic.

SWIFT wires, correspondent banks, and why the recipient can get less

A bank wire sent abroad rarely travels in a straight line. If your bank has no direct relationship with your recipient’s bank, which is common once the transfer crosses into a different country or a less-connected banking system, the payment is routed through one or more correspondent (or intermediary) banks that hold accounts for both sides and pass it along a chain, coordinated over the SWIFT messaging network. Each bank in that chain can deduct its own handling fee from the amount in transit before forwarding what’s left, often somewhere in the range of $15 to $50 per hop depending on the banks involved. That is why a wire can land in the recipient’s account short of what you actually sent, even when your own bank charged nothing at the counter.

Every SWIFT wire carries an instruction, field 71A (“details of charges”), that decides who absorbs those correspondent fees, and it’s worth knowing the three options exist:

- OUR — sender pays everything. Your bank collects every fee along the chain from you upfront, so the recipient is meant to receive the full invoiced amount. Even under OUR, though, the recipient’s own bank can still apply its own incoming-wire handling fee, which this option doesn’t control.

- SHA — shared, and the default at most banks. You pay only your own bank’s fee, and each correspondent along the way deducts its cut from the principal in transit, so the recipient can receive noticeably less than you sent, with no warning on your end.

- BEN — beneficiary pays everything. Every fee in the chain, including your own bank’s, is deducted from the principal, so the recipient receives the least of the three options.

None of this is exotic or unusual: it’s just how correspondent banking has worked for decades, and initiatives like SWIFT gpi have made it far easier to track a payment through the chain in real time, without changing the underlying fee structure. If it matters that your recipient gets the full amount, ask the sending bank to mark the transfer OUR rather than accepting whatever the default is, and confirm the option is even offered, since not every bank supports it for every corridor.

Compare the amount received, not the headline fee

The only fair way to compare two ways of sending money is the amount that actually lands in the recipient’s account, after every fee and every margin. A headline number like “$0 fee,” “low fee,” or “free transfers” describes one ingredient, not the finished dish. Two services can advertise the identical $0 fee and still deliver noticeably different amounts, because the whole difference sits in the rate. Reverse the received amount against the real mid-market rate at the moment you send, and the honest cost reveals itself, whatever the banner says.

Here’s how that plays out on an ordinary transfer. Say you’re sending $500 to a recipient in India, and at the moment you check, the mid-market rate is 83.50 rupees to the dollar, so at the honest midpoint, your $500 is worth 41,750 rupees. Put two typical routes side by side, each quoted on the number that matters: rupees that actually arrive.

| Route (illustrative) | Rate used | Rupees received | All-in cost | Cost vs mid |

|---|---|---|---|---|

| Bank wire, “$0 transfer fee” | 81.83 | 40,915 | 835 | 2.0% |

| Transfer app, $4 fee + near-mid rate | 83.25 | 41,292 | 458 | 1.1% |

Read the last two columns, not the sales pitch. The bank advertises no fee and still costs 835 rupees, because its whole margin lives inside a rate set roughly 2% below the mid. The app openly charges $4 and still delivers 377 more rupees, because its rate sits much closer to the real mid-market benchmark. The one that names a fee wins; the one that advertises “free” loses. That’s the entire point of reversing from the mid instead of trusting the banner.

These numbers are illustrative, not a quote: real rates move by the second and every provider prices differently by currency, corridor, amount and day. Run the same comparison with live figures at the moment you actually send, on your own corridor, and whichever route hands your recipient the most is the cheapest one, regardless of what its marketing calls itself.

Bank wire, transfer specialists, cash pickup, and card networks

The cheapest way to send money abroad depends on the amount, the corridor, and how your recipient will actually collect it. The table below is a starting map, not a ranking: every figure is typical and illustrative, not a quote, and it shifts with your provider, corridor and amount.

| Method | Typically cheap for | Watch out for |

|---|---|---|

| Bank wire (SWIFT) | Large, infrequent transfers, or when the recipient only has a traditional bank account and no other rail reaches them | Correspondent-bank fees along the chain, a wider margin on smaller amounts, and multi-day settlement |

| Money-transfer specialists (transfer apps) | Everyday and mid-size transfers, usually quoted near the mid-market rate with a transparent fee | Cash pickup, or certain corridors and currencies, can still carry a wider margin than the same provider’s digital bank-to-bank option |

| Cash pickup agents | A recipient with no bank account who needs cash the same day, through a wide network of physical locations | Often the priciest per dollar sent, particularly on thin corridors, because reach and speed cost more |

| Card networks / push-to-card | Quick, everyday transfers to a recipient with a debit card, usually settling fast | A card’s foreign-transaction fee, and any dynamic-currency-conversion prompt at the funding step, on top of the transfer’s own cost |

One pattern holds across the whole table: the visible price is rarely the whole price. A specialist’s advertised fee, a bank’s “no charge” wire, a cash agent’s flat counter fee: each is only part of the story until you add the margin sitting inside whatever rate was used. That’s also why the “best” method for a given amount can flip entirely once the corridor or the recipient’s collection method changes; a route that’s cheap for a bank deposit isn’t necessarily cheap for a cash pickup through the very same provider.

Stablecoins as a cheaper rail — and the real trade-offs

There’s a fifth rail worth understanding, even if it isn’t right for everyone: sending a stablecoin instead of a currency. A stablecoin is a token designed to track the value of a real currency, most commonly the US dollar, roughly one-for-one. In outline, it works like this: you convert your money into a stablecoin on an exchange, send that stablecoin directly to the recipient’s wallet over a blockchain network, and the recipient either holds it, spends it somewhere it’s accepted, or converts it back into local currency through an exchange or a local partner. The wallet-to-wallet leg itself typically settles in minutes, for a small network fee that generally doesn’t scale much with the amount sent.

The saving mostly comes from what’s missing. There’s no chain of correspondent banks, so nobody along the route deducts a per-hop handling fee, and the rate at each end is an ordinary trading spread rather than a bank’s retail margin. The IMF has pointed to exactly this: stablecoins can reduce the cost and increase the speed of remittances, particularly on corridors where the traditional cost runs highest, and some of the priciest corridors still cost close to a fifth of the amount sent, the traditional way. That’s the theoretical upside. Whether you actually see it depends heavily on the corridor, the platform, and the two moments where the money still touches the ordinary financial system.

Converting in and converting back out are where the real cost usually hides. Turning your home currency into a stablecoin, and turning it back into cash your recipient can spend, both involve an on-ramp or off-ramp: an exchange with its own trading fee and its own spread against the market rate. If either side is expensive, thin, or routes through an extra currency, the saving on the transfer itself can shrink or disappear entirely. Compare the whole round trip, entry to exit, not just the part that happens on the blockchain.

Hold the stablecoin yourself and you control it directly, with no intermediary and no help desk. Lose the private key or recovery phrase and there is typically no way to recover the funds; send to the wrong address and there is usually no reversing it. Leaving it on an exchange instead shifts that responsibility to the platform, along with the risk that the platform itself fails or is compromised.

This only holds for an asset actually designed to stay stable. Bitcoin, Ether and most other crypto assets are not pegged to any currency and can move sharply in either direction within a single day, which makes them a poor fit for moving a fixed sum someone is relying on to cover rent or a bill. If a stablecoin is what you mean by a “crypto transfer,” confirm that’s actually what’s being used before you send; a route that quietly substitutes a volatile token changes the risk completely.

What’s freely available, taxed a certain way, or fully legal where you live may be restricted or unavailable where your recipient lives, and the reverse is just as true; check a qualified local source before you rely on any of this. And because the rail is newer and less familiar, it draws a disproportionate share of scams: fake “support” asking for a recovery phrase, or a message demanding a fee to “unlock” funds that are supposedly already yours. No legitimate platform ever asks for either.

None of this makes stablecoins a magic fix. They’re one more option, with a genuinely different cost structure and a genuinely different set of risks, worth understanding before your next transfer rather than a replacement for comparing routes on the amount received.

Sign up with the code above for up to 20% off trading fees*. Whatever you decide, confirm the live rates, fees and availability on Binance’s own page first — and never share your password, 2FA code or recovery phrase.

*Up to 20% — you’ll see the exact figure on the Binance sign-up page. This is a sponsored referral link: it won’t cost you more, and the site may earn a commission. See our disclosure.

Habits that quietly cost more

A few ordinary habits inflate the cost of sending money abroad, and none of them look like a mistake at the time.

- Many small transfers instead of one larger one. Splitting a transfer into several smaller trips means each one absorbs its own flat fee and its own slice of margin, and the same total sent in five pieces usually costs more than sending it once. If timing allows, consolidate.

- Not comparing at all. Sticking with whichever bank or app you already have an account with, without ever pulling a competing quote, is the single most common way to overpay. Running the numbers through the conversion and pre-signup checklist before a transfer above pocket money takes a couple of minutes.

- Sending on a weekend or a holiday. Currency markets thin out when the underlying markets are closed, and a wider market spread tends to show up as a wider margin on whatever you send that day. If the transfer isn’t urgent, an ordinary weekday quote is usually the safer bet.

- DCC when funding a transfer by card. Paying into a transfer, or letting a recipient collect one, sometimes triggers dynamic currency conversion: a prompt to bill or credit in your home currency instead of the local one. It looks convenient and it’s usually the worst rate on the page; choose the local currency every time.

None of these habits are dramatic on their own, which is exactly why they’re easy to repeat. The fix is the same one that runs through this whole guide: compare the received amount, not the headline, and do it before you send rather than after. It’s the same discipline that matters when weighing a currency transfer against a crypto one: the cheapest route is whichever one actually delivers the most, not whichever one shouts the loudest.

Questions people ask

Why does a “$0 transfer fee” still cost me money?

Because the fee is only one of two costs. The other is the exchange-rate margin folded into the conversion, and it’s usually the larger of the two. A provider can waive the fee entirely and still take more than a competitor that charges a few dollars but prices the conversion close to the mid-market rate. Judge any offer by what actually lands in the recipient’s account, not by whether the fee line reads zero.

How do I find the real cost of sending money abroad?

Look up the mid-market rate for the currency pair at the moment you send, then compare it with the exact amount your recipient will receive after every fee and deduction. The gap between those two figures, expressed as a percentage, is the true all-in cost, regardless of what the provider’s marketing calls it.

Are banks or money-transfer specialists cheaper for sending money abroad?

It depends on the amount and the corridor, but broadly, banks tend to price a wider margin into an international wire, while specialist transfer services generally quote closer to the mid-market rate with the fee shown separately. On a large, infrequent transfer a bank can occasionally be competitive; for everyday amounts, specialists usually win. Compare the received amount on both before deciding.

Are stablecoin transfers actually cheaper than a bank wire?

They can be, mainly because there’s no chain of correspondent banks each taking a cut. But the saving depends on the fees and spread at the on-ramp and off-ramp, plus custody risk and rules that vary by country. Treat it as one option with real trade-offs, not an automatic discount.

Why did my recipient receive less money than I sent?

Most likely one of two things: the exchange-rate margin built into the conversion, or a correspondent-bank fee deducted somewhere along a SWIFT wire’s chain of intermediary banks. Depending on which “details of charges” option was used (OUR, SHA or BEN), those fees can fall on you, be shared, or fall entirely on the recipient.

What’s the cheapest way to send a large amount abroad?

There’s no single answer, because it depends on the currencies, the corridor and how the recipient will collect the money. But the routine is the same regardless: get the all-in received amount from two or three providers at the same moment, reverse each one against the mid-market rate, and send through whichever delivers the most. On a large sum, a fraction of a percent is real money.

- World Bank — Remittance Prices Worldwide, global average cost of sending remittances: remittanceprices.worldbank.org

- World Bank Data Blog — progress toward the UN SDG target on remittance costs: blogs.worldbank.org

- Financial Stability Board — G20 targets for enhancing cross-border payments, including remittance-cost targets: fsb.org

- Bank for International Settlements (CPMI) — correspondent banking and cross-border payment chains: bis.org

- International Monetary Fund — how stablecoins can affect payments and remittances: imf.org

Last updated 6 July 2026. This guide explains how the cost of sending money abroad breaks down and how to compare routes; it is not financial, tax or legal advice, and it doesn’t recommend any specific provider. Fees, margins, correspondent charges, regulation and availability differ by corridor and change constantly — confirm the live figures and local rules on the provider’s own page before you send.

Sign up with the code above for up to 20% off trading fees*. Whatever you decide, confirm the live rates, fees and availability on Binance’s own page first — and never share your password, 2FA code or recovery phrase.

*Up to 20% — you’ll see the exact figure on the Binance sign-up page. This is a sponsored referral link: it won’t cost you more, and the site may earn a commission. See our disclosure.