The rate you see is almost never the rate you get How the mid-market rate works, where the margin hides, and what a currency conversion really costs

If you’ve ever compared a “zero-fee” conversion to your bank’s and assumed the cheaper-looking one wins, this guide is for you. We’ll unpack the single most useful idea in foreign exchange (the mid-market rate) and show you how to measure what any conversion really costs, even when nobody charges a visible fee. It’s for anyone converting money, sending it abroad, or sizing up a broker. It is not a trading strategy, and it won’t tell you where rates are headed.

On this page

- The gist, in 30 seconds

- What the mid-market rate actually is

- Why your rate differs from Google

- The Mid-Rate Ruler: seeing the margin

- Why “zero fee” can be the expensive option

- Is “zero-fee” really free?

- How to measure the real cost

- A worked example: 1,000 EUR

- Costs by provider

- Dynamic currency conversion

- Why the gap varies

- Where the margin hides

- Sending money abroad

- What a fair margin looks like

- Where people lose money

- How to check the mid-rate yourself

- How the mid-rate is actually set

- Questions people ask

The gist, in 30 seconds

The mid-market rate (or “mid-rate”) is the midpoint between what the market will buy and sell a currency for: the honest reference price. Almost no one offers it to you directly. Instead, providers quote you a rate set slightly to one side, and the gap between their rate and the mid-rate is their margin. That margin, not the headline fee, is usually the biggest cost of a conversion. Learn to read any quote against the mid-rate and you can compare a bank, an app, a bureau and an exchange on the same honest footing.

What the mid-market rate actually is

At any moment, a currency has two live prices in the wholesale market: the highest price buyers are willing to pay (the bid) and the lowest price sellers will accept (the ask). The mid-market rate sits exactly between them. It is the number you see when you type “EUR to USD” into a search engine or look at a financial news ticker. It is real, but it is a wholesale price: the rate banks trade with each other in large size, not the rate offered to someone converting a few hundred dollars.

Think of it the way you think of any product with a wholesale and a retail price. The factory gate price of a coffee bag is not what you pay at the café. The mid-rate is the factory gate; the rate you’re quoted at the bank counter, in an app, or at an airport kiosk is the retail price. The difference between them is where the seller earns. With currency, that difference is built directly into the exchange rate, which is exactly why it’s so easy to miss.

Why the rate you get differs from the one on Google

Type “EUR to USD” into Google and you get a clean, confident number. Then you go to convert real money and the figure is worse. Nobody made a mistake, and nobody is necessarily overcharging you. The two numbers are answering different questions.

The rate Google shows is the mid-market rate: the interbank benchmark, the midpoint between the wholesale buy and sell prices that large banks quote each other. It is the reference the whole market agrees to point at. What it is not is a price you or I can transact at. Banks trade with each other in millions at a time, and that scale is what earns the wholesale price. Nobody at the counter is going to hand a tourist the rate reserved for a seven-figure trade between two banks.

So your provider — the bank, the app, the bureau — starts from that mid-rate and quotes you a retail rate set a little to one side. If you’re buying dollars, the rate they give you buys slightly fewer dollars than the mid would. That gap is the margin, and it’s where the provider earns. On the Mid-Rate Ruler above, Google is standing at the mid mark; your quote is the mark a short distance away, and the shaded band between them is the difference you pay.

There’s a second, smaller reason the numbers disagree: timing. The mid-rate moves every second of every trading day, but the figure on a search page is a snapshot, often lagging the live market by seconds or minutes. For a major pair on a calm afternoon that lag is trivial. Around a news release, or on a currency that trades thinly, it can be enough to notice. A rate you screenshot at breakfast is not the rate on offer at lunch.

Put those together and the picture is straightforward. Google gives you the honest wholesale benchmark, delayed a little. Your provider gives you a live retail price with their cut built into it. The distance between the two, at the same moment, is the real cost of the conversion: not the delay, and not any headline fee they may also charge.

This is why the mid-rate is worth knowing rather than ignoring. It won’t be the rate you get, but it’s the only fixed point that lets you judge the rate you’re offered. Without it, “1.0610” is just a number on a screen. With it, you can see that 1.0610 against a 1.0850 mid is a roughly 2.2% margin, and decide whether that’s reasonable or whether the next provider does better. The search rate is your starting line, not your finish line.

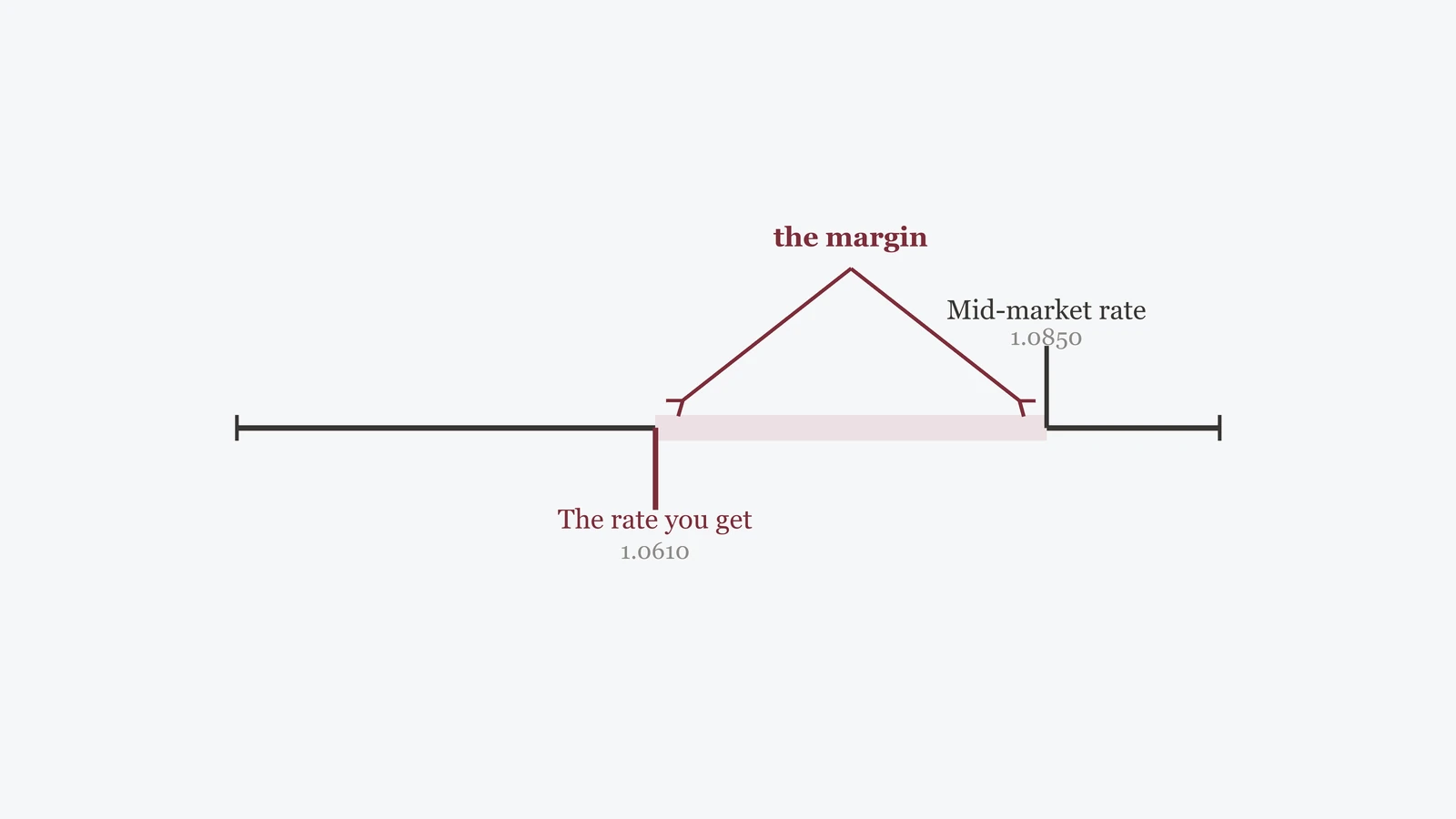

The Mid-Rate Ruler: seeing the margin

Here is the picture we’ll come back to throughout these guides. Put the mid-market rate on a line. Then mark the rate you’re actually offered. The distance between the two is the margin: the provider’s cut, baked into the rate with no separate line item.

Numbers are illustrative, not a quote. Real rates and margins change every second — always read the provider’s live screen.

In the example, the mid-rate is 1.0850 but you’re offered 1.0610. On a conversion, that roughly 2.2% gap is the true cost, whether or not the provider also lists a flat fee. Once you can see the ruler, every “great rate, no fees!” ad becomes a question: a great rate compared to what?

Why “zero fee” can be the expensive option

A flat fee is honest in one sense: you can see it. A margin is quieter, because it’s expressed as a slightly worse exchange rate, and most people have no reference point to judge it against. So a provider can advertise “no fees” truthfully while charging more than a competitor that lists a small flat fee but uses a rate much closer to the mid.

The lesson isn’t “fees are good.” It’s that the headline fee and the headline rate are two different costs, and you have to add both. A “1.5% fee at the mid-rate” can easily beat “no fee” at a rate that’s 3% off the mid. The only way to know is to put both on the ruler.

Is “zero-fee” currency exchange ever really free?

“No fees” is usually a true statement. It just isn’t the whole sentence. A provider can charge you nothing that looks like a fee and still make good money on the conversion, because the earnings are folded into the exchange rate rather than itemised anywhere you’d spot them. The claim is accurate; the cost is real; both things are true at once.

Here’s the mechanism in practice. When your bank or card converts a purchase abroad, it typically applies a markup to the mid-rate, often somewhere around 1% to 3% for ordinary currencies, and higher still on exotic ones or on physical cash. You never see a line called “markup.” You just receive slightly fewer of the target currency than the mid would have given you. Multiply that by every holiday, every online order in another currency, every subscription billed abroad, and the “free” conversions add up to a quiet, steady cost.

Multi-currency apps of the Wise or Revolut type get much closer to the mid, which is why they feel almost free by comparison. But “close to the mid” is not “the mid.” They still take a small explicit fee, or ride a slim spread, or both. And on weekends or thinly traded pairs that spread can widen. A card scheme is similar: the Visa or Mastercard network rate used for cross-border purchases is very good, but it isn’t exactly the interbank mid, and your own bank may add its foreign-transaction fee on top of it.

None of this means the free-sounding options are traps. Often they’re genuinely the cheapest thing available. It means the word “free” tells you nothing until you’ve put the rate on the ruler. Two providers can both advertise no fees and cost you very different amounts, and the only way to rank them is to reverse the all-in figure from the mid, as in the steps below.

A retail rate within roughly 1% of the mid is competitive for a common pair. Past that, treat “no fees” as a marketing line, not a price, and check what you’d actually receive somewhere else before you commit.

How to measure the real cost of any conversion

You don’t need finance training for this: just two numbers and a calculator.

- Find the live mid-market rate for your pair from a neutral source (see the last section). Write it down with the time, because it moves.

- Get the provider’s “all-in” figure: how much of the target currency you’ll actually receive for your amount, after every fee.

- Work out what you would have received at the mid-rate (your amount × the mid-rate).

- Subtract: mid-rate result minus what you’re actually getting. That difference is the total cost: margin plus fees combined.

- Divide that cost by the mid-rate result to express it as a percentage. Now you can compare any two providers, in any currencies, on one honest scale.

This “reverse from the mid-rate” method is the whole trick. It folds the visible fee and the invisible margin into a single, comparable number.

A worked example: converting 1,000 EUR to USD

Suppose the mid-rate is 1.0850, so 1,000 EUR is worth 1,085.00 USD at the honest midpoint. Here’s how three made-up providers might compare once you reverse everything from the mid:

| Provider (illustrative) | USD received | Total cost | Cost vs mid |

|---|---|---|---|

| “No fees” app, rate 1.0610 | 1,061.00 | 24.00 | 2.2% |

| Flat fee, rate near mid 1.0835 | 1,075.50 | 9.50 | 0.9% |

| Airport bureau, rate 1.0250 | 1,025.00 | 60.00 | 5.5% |

The “no fees” option costs more than twice the one that charges a visible fee, and the bureau costs nearly six times as much, all without a single dishonest claim. These are illustrative numbers to show the method, not real quotes; the point is the comparison, not the figures.

What a conversion costs at each kind of provider

The ruler is the same everywhere, but different providers sit at very different marks on it. The table below gives typical, illustrative cost ranges — measured as the total gap from the mid-rate, fees and margin combined — so you can see roughly where each kind of provider tends to land. Actual figures vary by currency, amount, day and country, so treat these as a map, not a quote.

| Method | Typical all-in cost vs mid | Best for | Watch out for |

|---|---|---|---|

| High-street bank counter or transfer | ~2%–5% | People who value the branch and don’t mind paying for it | Margin baked into the rate; a “free” transfer can still be pricey |

| Debit or credit card abroad | ~1%–3% | Everyday spending on trips; convenience | Foreign-transaction fee on top of the network rate; cash advances on credit cards cost more |

| Multi-currency app (Wise / Revolut-type) | ~0.3%–1% | Regular converters who want close-to-mid pricing | Small fee or spread; weekend and exotic-pair markups; plan limits |

| Airport or tourist bureau | ~5%–12% | A genuine last-minute cash emergency, nothing more | The widest margins on the high street; “0% commission” hides it in the rate |

| ATM abroad | ~1%–3% + fees | Getting local cash when you need it | Operator fee, your bank’s fee, and the DCC trap at the keypad |

| Crypto exchange | Spread + fee (varies) | Converting to or from digital assets | Same ruler applies; check the live spread and fee before you trade |

A few of these deserve a word beyond the table. The high-street bank is the default many people never question, and it’s rarely the cheapest. The convenience of the branch and the brand is paid for in the rate. That can be an acceptable trade if you value the counter, but it’s worth knowing you’re making it.

Cards abroad are usually fine for everyday spending, provided you understand the two layers: the good network rate, and a foreign-transaction fee your bank may add on top. Some cards charge nothing extra; some charge a few percent. It’s worth checking yours once, before a trip, rather than discovering it on the statement afterwards.

Multi-currency apps sit closest to the mid and are hard to beat for regular, mid-sized conversions. They earn their keep on a slim fee or spread, and the honest ones show you the fee plainly. The catch is the edges: weekends, holidays and thinly traded currencies, when the spread widens quietly.

The airport bureau is the outlier at the expensive end, and the “0% commission” sign is exactly why — with no commission line, the entire cost lives in a rate set far from the mid. It earns its place only in a real cash emergency. An ATM abroad is usually much better, but it stacks fees: the machine operator’s charge, your own bank’s foreign-cash fee, and the dynamic-currency-conversion offer at the keypad, covered next. A crypto exchange plays by the same rules as any FX venue — there’s a spread between buy and sell, sometimes a fee alongside it, and the ruler measures both. If you’re comparing one, read the live spread and fee on the exchange’s own page rather than trusting a headline.

Dynamic currency conversion: why “pay in your own currency?” costs you

You’re at a card terminal in another country, or at a foreign ATM, and the screen asks a friendly-looking question: would you like to pay in your home currency instead of the local one? The button that says “yes, my currency” is dynamic currency conversion, and pressing it usually costs you money.

Here’s what happens behind that button. Choose the local currency, and the conversion is handled later by your own card network (Visa or Mastercard) at their rate, which sits close to the mid. Choose your home currency, and the merchant’s terminal or the ATM operator does the conversion instead, at a rate they set. That rate is typically 3% to 5% worse than the network would have given you, and sometimes more. Worse, it’s applied on top of any foreign-transaction fee your bank charges, so you can end up paying twice.

The reason DCC looks appealing is genuinely clever design. Seeing the total in your own currency feels reassuring — no mental arithmetic, no surprise on the statement, a number you understand. That comfort is precisely what you’re paying for. The home-currency figure on the screen already has the poor rate baked in; it looks certain because the cost has been hidden inside it. The local-currency figure looks unfamiliar only because the fair conversion hasn’t happened yet.

The habit worth building is simple, and it almost always saves money: pay in the local currency. If you’re in Spain, pay in euros; in Japan, pay in yen. Let your own bank or card network do the conversion. The one time the home-currency figure is useful is as a rough sanity check — glance at it, then choose local anyway. And if a terminal converts to your currency automatically without asking, you’re usually entitled to ask for the charge in the local currency instead.

At any foreign terminal or ATM, always pick the local currency. Paying in your home currency hands the conversion to the merchant at a rate they set — typically several percent worse than your own card network’s.

Why the gap is wider on some currencies — and some days

The same conversion doesn’t cost the same everywhere or at every hour. If your rate looks unusually bad, the currency and the timing often explain most of it, and knowing why saves you from blaming the wrong thing.

Start with the currency. The deeply liquid majors — EUR/USD, USD/JPY, GBP/USD — trade in enormous volume around the clock, so the interbank market for them is thick with buyers and sellers. That depth keeps the spread between bid and ask tight, which keeps the margin small. There’s so much competition that no single provider can drift far from the mid without losing business.

Exotic and emerging-market currencies are the opposite. Fewer participants trade them, the wholesale market is thinner, and the bid-ask spread is naturally wider — so the retail margin built on top of it is wider too. A conversion that costs a fraction of a percent in EUR/USD can cost several percent in a thinly traded pair, before any provider adds a markup. Physical cash in those currencies is wider again, because someone has to hold, ship and insure the notes.

Then there’s timing, which catches people out because their need to convert doesn’t stop for the weekend. The interbank market is busiest when the big financial centres overlap; liquidity thins in the small hours, on public holidays, and across the weekend when much of the wholesale market is closed. Thinner liquidity means wider spreads, so a Saturday conversion (especially through an app that quotes a live weekend rate) often carries a visibly bigger margin than the same conversion on a Tuesday afternoon. Providers know the weekend rate can move before markets reopen, and they price that risk into the spread.

Scheduled news adds a sharper, briefer version of the same effect. Around a central-bank decision or a major data release, prices can move fast and liquidity can vanish for minutes, so spreads gap wide right when everyone wants to trade. Converting in the middle of that window rarely gets you a good number.

Amount matters as well. On a small conversion, a flat fee eats a large share of the total, and some providers also widen the percentage margin on tiny amounts because they aren’t worth much to them at a fair rate. The upshot is that fifty units of an exotic currency, in cash, on a Sunday, is close to the worst-case corner of every dimension at once — and a large electronic conversion of a major pair, mid-week, is close to the best.

One structural detail is worth naming, because it explains a lot of bad exotic-currency rates. Two currencies that don’t trade directly against each other in size are often converted through the US dollar behind the scenes — say from one small currency into dollars, then dollars into another. Each leg carries its own spread, so the pair inherits the cost of two conversions rather than one. That is a big part of why an exotic-to-exotic conversion can look punishing even when neither currency, on its own, is especially illiquid.

Two habits follow from all this. First, if you have any flexibility on when you convert, favour mid-week during main trading hours over a weekend or a holiday — the difference on a thinly traded currency can be real money. Second, before you accept a weekend or exotic quote, check whether the provider is showing a live rate or a “weekend rate” with an extra buffer baked in, and get a second quote to compare. The gap is legitimately wider in these conditions, but “wider” still varies a lot between providers, and that variation is where your shopping pays off.

When you must convert an exotic currency, or convert on a weekend or holiday, the gap is structurally larger — not a rip-off, just thinner liquidity. Shop harder, get two or three all-in quotes, and don’t judge the number against a EUR/USD yardstick.

Where the margin hides: four places to look

Once you’re looking for it, the margin shows up in predictable spots:

- Inside the rate. The most common hiding place. The quoted rate is simply set away from the mid.

- In a percentage “fee” that’s really a markup. Some providers split the cost into a small flat fee plus a percentage that quietly widens on smaller or exotic currencies.

- In “dynamic currency conversion.” When a card terminal or website offers to charge you in your home currency, it’s usually applying its own poor rate. Paying in the local currency and letting your own bank convert is often cheaper.

- In the spread on a trading screen. On a broker or exchange, the buy and sell prices straddle the mid. The wider that spread, the more you pay to get in and out.

Sending money abroad: the same ruler, a few extra costs

Sending money to another country runs on exactly the margin logic we’ve been using: there’s a mid-rate, and the service quotes you a rate set to one side of it. What changes with a transfer is that a handful of extra costs stack on top of that margin, and they’re easy to miss if you only look at the advertised fee.

The first is an explicit transfer fee, which most services show up front — the honest, visible part of the bill. The second hides in the old correspondent-banking system: a traditional SWIFT transfer can pass through one or two intermediary banks on its way, and each can shave off a charge, so the amount that lands can be less than the sender was quoted. The third is a speed premium: paying for an instant or same-day transfer often costs more than letting a standard one arrive in a couple of days.

Because those costs pile up in different places, the advertised fee is a poor way to compare services. The reliable method is to reverse from the mid, as before — but from the recipient’s side. Ask a single question of each service: for the amount I’m sending, how much will actually arrive in the recipient’s account? Compare that landed figure against what the mid-rate would deliver, and every fee, margin and intermediary charge collapses into one honest number you can rank.

One trap deserves a flag: a transfer that involves two conversions. Sending from a currency the service doesn’t hold directly to a currency it doesn’t pay out directly can route through a third currency — converting twice, and charging a margin each time. Two conversions can roughly double the currency cost of the transfer for no benefit to you. Where you can, send in a way that converts once, and always judge by the amount that reaches the other end.

What a fair margin looks like — and when to walk away

There is no universal “fair” number, because it depends on the currencies, the amount, the method and where you are. A common, liquid pair moved in a normal way should cost far less than a thinly traded currency converted in cash at a tourist counter. The point of the ruler isn’t to memorize a threshold; it’s to compare like for like and notice when one option is an outlier.

If you can’t find the mid-rate, you can’t judge the offer. Treat “great rates” with no reference point the same way you’d treat a sale price with the original price hidden.

Walk away if a provider won’t show the all-in amount you’ll receive before you commit, pressures you to decide instantly, or asks you to pay an extra “release” or “unlock” fee to access money that’s supposedly yours. Those are not pricing quirks; they are red flags.

Where people lose money

Three errors cost people the most:

- Comparing rates at different times. Rates move constantly. A quote from this morning isn’t comparable to one from now. Compare both against the mid at the same moment.

- Judging by the fee alone. “No fee” tells you nothing until you know the rate. Add both costs, always.

- Ignoring the amount. A flat fee barely matters on a large transfer but dominates a small one; a percentage margin does the opposite. The cheapest option for $50 may be the priciest for $5,000.

How to check the mid-rate yourself

Do this once and it becomes second nature. Open a neutral rate source and read the current mid for your pair, noting the time. Central banks publish reference rates you can sanity-check against — the European Central Bank, for instance, publishes daily euro reference rates — and the broader structure of the FX market is documented by the Bank for International Settlements. Then take any provider’s all-in figure and reverse it from that mid, exactly as in the steps above. If a provider’s rate is wildly off the published reference, that’s your signal to look closer.

How the mid-rate is actually set

It helps to know where that midpoint comes from, because “the market’s honest price” sounds like a committee sits somewhere and publishes it. Nobody does. The mid is a byproduct of a live wholesale market called the interbank market, and once you picture that market the number stops being mysterious.

Here is the plumbing, stripped of jargon. A handful of very large banks — the ones you’d recognise — stand ready to buy and sell major currencies against each other all day. Each quotes two prices to the others: a price it will buy at and a slightly higher price it will sell at. When one bank’s selling price meets another’s buying price, a trade happens, and the size of these trades is enormous by retail standards. The mid-rate you see on a search page is simply the midpoint of the best of those quotes at that instant. No one sets it deliberately; it falls out of thousands of banks and trading firms leaning against each other for the best price.

That is also why it never sits still. Every large order, every shift in interest-rate expectations, every headline nudges the balance of who wants to buy and who wants to sell, and the midpoint slides to follow. On EUR/USD in the middle of a busy trading day the number can change many times a second. It is not being updated by anyone — it is the running score of a continuous auction.

The part worth internalising is who gets to trade at those prices, because it explains the margin on your own conversions. The wholesale rate is earned by size. A bank dealing in millions at a time is a counterparty another bank wants; a person changing a few hundred dollars is not, and could not settle a trade in that market even if allowed to. So the retail chain exists precisely to bridge that gap: your bank or app trades in the wholesale market on its own account, then passes currency down to you at a retail price set to one side of the mid. You are buying the wholesale rate at second hand, with the middleman’s cut folded into the number — which is the margin the rest of this guide is about.

One practical consequence follows. Because the mid is a wholesale auction price, no ordinary provider can quote you exactly the mid and stay in business — they’d be selling at cost with staff, licences and risk to pay for. The honest ones get close to it and charge a small, visible fee; the expensive ones sit far from it and call the difference nothing. Knowing the number is an auction result, not a posted price, is what lets you treat every retail quote as a markup on a wholesale figure you can actually look up.

Questions people ask

Is the mid-market rate something I can actually get?

Rarely, and usually only as a large institution. For ordinary conversions it’s a benchmark, not an offer. Some providers get close to it and charge a transparent fee; that’s often the better deal.

Why does the mid-rate keep changing?

Because currencies trade continuously and their prices respond to supply, demand, interest rates and news. See what moves an exchange rate for the forces behind it.

Is a tighter spread always cheaper?

A tighter spread helps, but it’s only one part of the cost. A tight spread paired with a rate set far from the mid can still be expensive. Always reverse the all-in figure from the mid.

Does this apply to crypto exchanges too?

Yes. Buying or converting on an exchange has a spread and sometimes a fee, exactly like FX. The same ruler works. If you’re comparing one, check the live numbers on Binance’s own fee page first.

Why is my bank’s rate worse than Google’s?

Google shows the mid-market rate — the wholesale benchmark banks trade at among themselves. Your bank quotes a retail rate set a little to one side, and that gap is its margin. The bank’s rate isn’t an error; it’s the price with their cut built in. Reverse the all-in figure from the mid to see the real difference.

Should I pay in local or home currency when abroad?

Always local. Paying in your home currency triggers dynamic currency conversion, where the merchant or ATM converts at a rate they set — typically 3% to 5% worse than your own card network’s, and often on top of a foreign-transaction fee. The home-currency total looks reassuring because the poor rate is already hidden inside it.

How much markup is too much?

For a common, liquid pair, a retail rate within about 1% of the mid is competitive. Somewhere around 2% to 3% is common at banks and cards but usually beatable. Past roughly 5% — typical of airport bureaus — you’re paying a lot. There’s no fixed line; compare against the mid and against one alternative.

Is Wise or Revolut really the mid-market rate?

Close, but not exactly. Multi-currency apps of that type get much nearer the mid than a bank does, then take a small, usually visible fee or a slim spread. On weekends, holidays or thinly traded currencies that spread can widen. They’re often the cheapest option — just check the fee, don’t assume it’s zero.

What’s the cheapest way to convert a large amount?

On big amounts a percentage margin matters far more than a flat fee, so the priority is a rate close to the mid. Multi-currency apps or a specialist FX service usually beat a bank counter. Get the all-in landed figure from two or three providers at the same moment and compare each against the mid.

Are airport currency booths ever worth it?

Only in a genuine cash emergency. Airport and tourist bureaus carry the widest margins on the high street, often 5% to 12%, and the “0% commission” sign just means the whole cost is hidden in the rate. If you have any other option — an ATM, a card, an app — it will almost always cost you less.

- European Central Bank — euro foreign-exchange reference rates: ecb.europa.eu

- Bank for International Settlements — Triennial Survey of FX market structure: bis.org

- International Monetary Fund — exchange-rate concepts and data: imf.org

Last updated 6 July 2026. This guide explains pricing concepts and how to compare conversions; it is not investment, tax or legal advice. Specific rates, fees and availability are set by each provider and change constantly — always confirm the live figures on the provider’s own page.

Sign up with the code above for up to 20% off trading fees*. Whatever you decide, confirm the live rates, fees and availability on Binance’s own page first — and never share your password, 2FA code or recovery phrase.

*Up to 20% — you’ll see the exact figure on the Binance sign-up page. This is a sponsored referral link: it won’t cost you more, and the site may earn a commission. See our disclosure.