Why there are two prices, and you always get the worse one Bid, ask and the spread: what they are, why they widen, and what they cost you

If you’ve ever glanced at a currency app or a broker screen, seen a “buy” price and a “sell” price sitting side by side, and wondered why they’re different — this guide is for you. We’ll explain the bid, the ask, and the spread between them in plain English, show you why the gap exists and when it gets wider, and work out what it actually costs you. It is not a trading method and it won’t tell you where any price is going.

On this page

- Quick version

- What the bid is

- What the ask is

- The spread: the gap, and who earns it

- Why two prices exist at all

- How bid and ask straddle the mid-rate

- How to read a spread on a screen

- When spreads get wider

- Spread vs a separate commission

- The round-trip cost

- Easy ways to get this wrong

- Commission and spread: adding both up

- Dealer pricing vs an ECN

- Slippage: when you don’t get the price you saw

- Putting a number on the spread

- Questions people ask

Quick version

A currency doesn’t have one price — it has two at the same instant. The bid is the price someone will buy from you (the price you sell at); the ask is the price someone will sell to you (the price you buy at). The ask is always a little higher than the bid, and the gap between them is the spread. That spread is a cost you pay simply for the privilege of trading, and it’s collected by the firms that stand ready to deal on both sides. Whenever you trade, you take the worse of the two prices — and if you go in and come back out, you cross the spread twice.

What the bid is

The bid is the highest price a buyer is currently willing to pay for a currency. If you are the one selling — converting euros back into dollars, say, or closing a position — the bid is the price you get. It is the “we’ll take it off your hands for this much” number. Crucially, it’s always the lower of the two prices on the screen. When you sell, you sell at the bid, and the bid is never the best-looking number in the quote.

What the ask is

The ask — sometimes called the offer — is the lowest price a seller will accept to hand the currency over. When you are buying, the ask is your price. It is the “you can have it for this much” number, and it always sits a touch above the bid. So the rule is simple and a little annoying: you buy at the higher ask and sell at the lower bid. Either direction, the price that applies to you is the one that’s slightly worse than the one in the middle.

The spread: the gap, and who earns it

The spread is just the distance between the bid and the ask. If a pair is quoted 1.0848 / 1.0852, the spread is four units in the last decimal place (often called “pips”). That gap is not an accident or a glitch — it is the price of doing business, and it goes to whoever is quoting both sides. Think of it the way a currency bureau works: the airport kiosk will sell you euros at one rate and buy them back at a worse one, and the difference between its two posted prices is how it makes money. The spread on a screen is the same idea, just narrower and updated every fraction of a second.

Why two prices exist at all

Two prices exist because someone has to stand in the middle and be willing to trade with you the instant you decide to act. These firms — market makers, or liquidity providers — quote a price they’ll buy at and a price they’ll sell at, and they hold the currency in between. They carry the risk that the price moves against them while they’re holding it, and they handle the work of matching buyers and sellers who don’t arrive at the same moment. The spread is their compensation for providing that always-on availability. The wholesale market works exactly this way; the retail prices you see are the same mechanism passed down a layer, with a little more width added on.

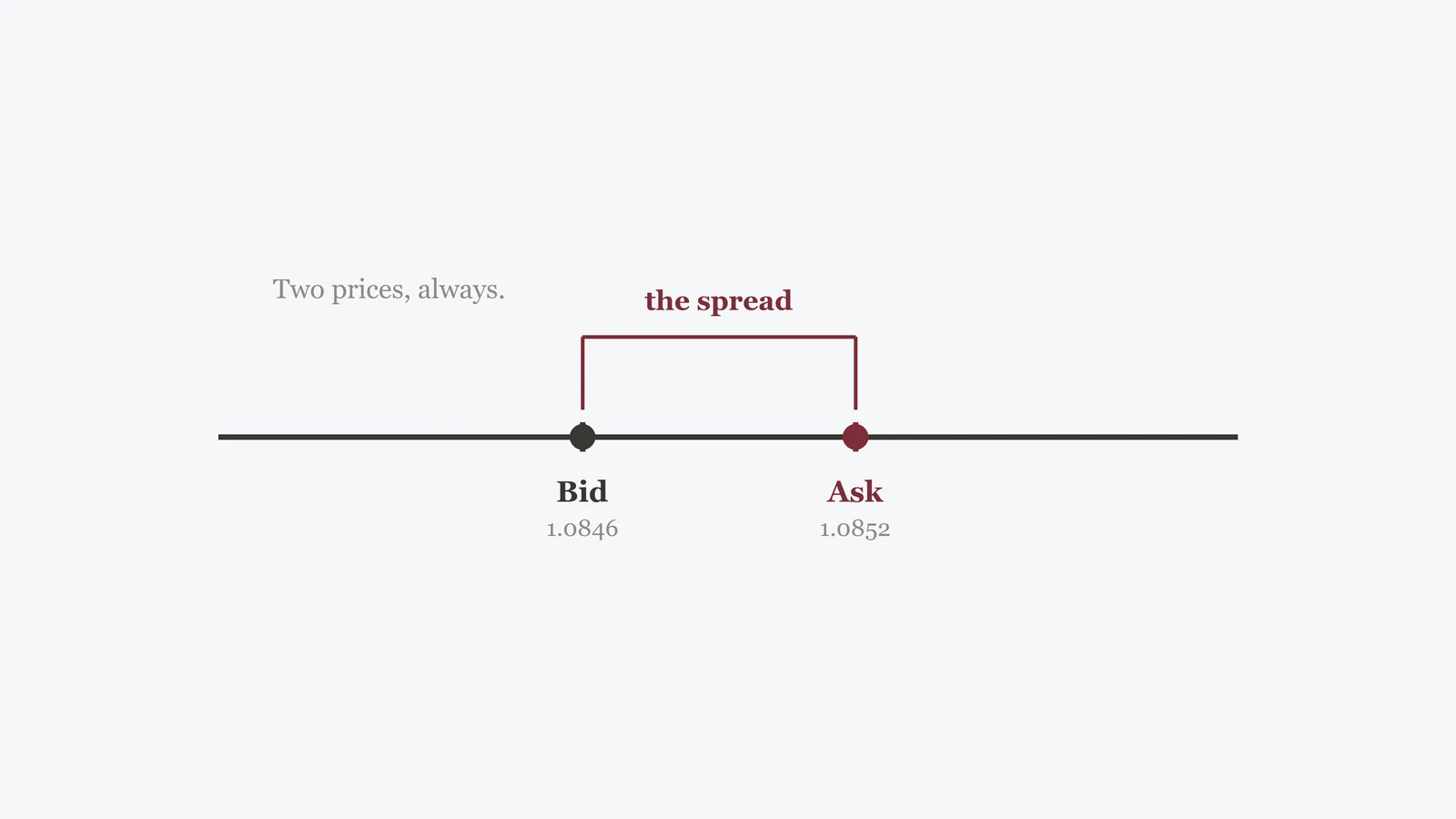

How bid and ask straddle the mid-rate

If you average the bid and the ask, you land on the midpoint — the mid-market rate. That mid is the honest reference price, the number a search engine shows you, but it’s a price almost nobody actually trades at. The real quotes sit either side of it: the bid just below, the ask just above. Picturing the two prices on a line, with the mid in the centre, is the clearest way to see what a spread costs you.

Numbers are illustrative, not a quote. Real bids, asks and spreads change every second — always read the provider’s live screen.

In the picture, the mid is 1.0850, the bid is 1.0848 and the ask is 1.0852. You’d buy at 1.0852 and sell at 1.0848 — never at the tidy 1.0850 in the middle. The wider those outer marks sit from the centre, the more the spread is taking from you.

How to read a spread on a screen

Quotes look intimidating until you know which number is which. Here’s how to decode any of them.

- Find the two prices. They’re usually shown as a pair — often labelled “Sell / Buy” or “Bid / Ask” — or as a single quote like 1.0848 / 1.0852.

- The lower number is the bid (your selling price). The higher number is the ask (your buying price).

- Subtract the bid from the ask. That difference is the spread — the gap you pay to trade.

- Compare the spread to the mid-rate to judge it: a few units on a major pair is normal; a wide gap on an obscure pair or at an odd hour is a sign of thin trading.

- Remember which side applies to you. Buying? Use the ask. Selling? Use the bid. Never assume you get the number in the middle.

When spreads get wider

A spread is not fixed; it breathes with the market. It tends to widen in a few predictable situations, and knowing them helps you avoid trading at the worst moments.

| Situation (illustrative) | Typical spread | Why |

|---|---|---|

| Major pair, busy session | Narrow | Deep liquidity, many firms competing to quote |

| Exotic or thinly traded pair | Wide | Few buyers and sellers, more risk to hold |

| During a major news release | Wide | Prices jump; firms widen to protect themselves |

| Weekend or after-hours | Wide | Thin liquidity when main markets are closed |

Spreads on widely traded pairs in active hours are usually narrow because many firms compete to quote them. The moment liquidity thins — an unusual currency, a quiet hour, the seconds around a central-bank announcement — the gap can open up sharply. The figures above are illustrative to show the pattern, not real quotes.

Spread vs a separate commission

The spread is one way you pay; a commission is another. Some providers fold their entire charge into a slightly wider spread and advertise “no commission.” Others quote a tighter, near-wholesale spread but add a separate commission line. Neither is automatically cheaper — you have to add both together. A tight spread with a commission can easily beat a “commission-free” quote whose spread is doing all the quiet work. The only honest comparison is the all-in cost: spread plus any commission, measured against the mid-rate.

The round-trip cost: you cross the spread twice

Here’s the part that catches people out. You don’t pay the spread once — you pay it on the way in and again on the way out. To open a position you buy at the higher ask; to close it you sell at the lower bid. Even if the mid-rate hasn’t moved at all, you come back to where you started having paid the full spread, because you bought high and sold low by exactly that gap.

The price has to move in your favour by at least the full spread before a round trip even breaks even. On a wide spread, or a pair you trade in and out of often, that cost adds up quietly. The narrower the spread and the fewer the round trips, the less it drains.

This is why frequent in-and-out activity is more expensive than it looks: every round trip is a fresh crossing of the spread, whether or not the market did anything at all.

Easy ways to get this wrong

Three errors cost people the most when they first meet a two-sided quote:

- Assuming you get the mid-rate. The number in a search engine is the midpoint. You trade at the bid or the ask, never the middle — so a quote will always look a little worse than the rate you looked up.

- Counting the spread only once. A round trip crosses it twice. If you plan to get out as well as in, double the cost in your head.

- Ignoring the spread on “commission-free” offers. “No commission” doesn’t mean no cost. The charge may simply be living inside a wider spread. Add both, always.

Be wary of anyone advertising a “zero spread” or “no-cost” quote without showing where the cost actually is — a hidden commission or a poor rate is usually doing the work instead. Walk away from anyone who pressures you to trade instantly before you’ve seen the all-in figure, or who hides the second price until after you’ve committed. Those are not pricing quirks; they are warning signs.

Commission and spread: adding both up

Earlier we said the only honest comparison is the all-in cost. That is easy to write and easy to get wrong, because the two charges are quoted in different shapes. A spread is baked into the price you trade at; a commission is a flat line billed on the side, often per lot or per amount converted. To compare two providers fairly you have to drag both onto the same ruler, and the ruler is always the mid-rate.

The method is plain. Take the spread and turn it into a cash figure for the exact amount you plan to trade. Take the commission and turn it into a cash figure for that same amount. Add them. Do the same for the rival quote. Whichever total is smaller is the cheaper deal — regardless of which one shouted “commission-free” on the tin.

A worked comparison shows how easily the headline misleads. Say you are converting the equivalent of 10,000 units and you have two quotes, both illustrative:

| Provider (illustrative) | Spread cost | Commission | All-in |

|---|---|---|---|

| A — “commission-free,” wider spread | ~25 units | 0 | ~25 units |

| B — tight spread, flat commission | ~8 units | ~10 units | ~18 units |

Provider A looks friendlier because there is no commission line to flinch at. But once the spread is priced in cash, its wider gap does more damage than B’s tight spread plus a modest fee. On this illustrative amount B is cheaper by roughly a third, even though it is the one that charges a visible commission. Flip the trade size, though, and the answer can flip too: a flat commission hurts proportionally more on tiny trades and matters less on large ones, while a spread scales with the amount either way. So the comparison is worth redoing for the size you actually deal, not just once in the abstract.

Two practical cautions. First, make sure you are comparing the same amount and the same pair — a spread quoted on a busy major is not comparable to one on a thin exotic. Second, watch for charges that live outside both the spread and the commission: a deposit fee, a withdrawal fee, an inactivity fee. Those do not show up in either column above, but they still come out of your pocket, so the truly all-in figure includes them.

Dealer pricing vs an ECN

Where a quote comes from shapes how fair it is likely to be, and there are broadly two arrangements behind the screen. The labels sound technical, but the difference is one you can feel in the price.

A dealer, or market maker, quotes its own two-sided price and takes the other side of your trade itself. When you buy, it sells to you; when you sell, it buys from you. It is not passing your order out to a wider market — it is the counterparty. That is a legitimate model and it can offer steady, predictable spreads, but it carries a structural tension: the firm setting your price also profits from the spread you pay, and in some setups from your losses. When a market moves fast, a dealer may also requote — decline your click at the shown price and offer a new, worse one — because it does not want to fill you at a number that has already gone stale.

An ECN, or electronic communication network, works the other way. Rather than quoting its own price, it aggregates live quotes from many banks and other participants and shows you the best available bid and ask from that pool. Your order is matched against a real counterparty in the network, not against the venue itself. Spreads on an ECN are often tighter, especially on liquid pairs, because many providers are competing; the venue typically earns a transparent commission instead of a marked-up spread. The trade-off is that ECN spreads are variable — they can widen noticeably when the underlying pool thins.

Neither arrangement is automatically the right one, and plenty of retail providers sit somewhere in between or route different orders differently. The point is to know which you are dealing with, because it tells you what to watch. With a dealer, the thing to check is whether the spread is fair and whether requotes bite in fast markets. With an ECN, the thing to check is the commission and how far the spread stretches when liquidity dries up. If a provider will not tell you plainly how it makes money from your trade, treat that reticence as information in itself.

Slippage: when you don’t get the price you saw

The spread explains the gap between the two prices at a single instant. Slippage is a different problem: the gap between the price you saw when you clicked and the price you actually got. On a calm day in a liquid pair the two are almost identical. In fast or thin conditions they can drift apart, and the drift is not always in your favour.

It happens because a market order asks to be filled at the best price available right now, not at a price you have locked in. Between the moment you tap and the moment the order reaches the market, prices keep moving. If they have moved against you in those fractions of a second — or if there simply is not enough size resting at the quoted level to fill your whole order — you get filled at the next available price, which is worse. Three conditions make it more likely:

- News and gaps. Around a major release, or when a market reopens after a weekend, prices can jump from one level to another with nothing traded in between. A market order landing in that gap fills wherever the price has jumped to, not where it was.

- Order size. A large order can exhaust the quotes sitting at the best price and eat into worse ones behind them, so the average fill is poorer than the top-of-book number you saw.

- Thin liquidity. An exotic pair, a quiet hour, or a stressed market has fewer resting orders, so even a modest trade can move through several price levels.

The usual trade-off is a limit order. Instead of “fill me at whatever is going,” a limit order says “fill me at this price or better, and not worse.” That protects you from a bad fill — but it introduces the opposite risk: if the market never reaches your price, or gaps straight past it, your order may not execute at all. A market order trades certainty of execution for uncertainty of price; a limit order trades certainty of price for uncertainty of execution. Which you want depends on whether getting done matters more to you than the exact number, and that changes trade to trade.

Slippage is not a sign that something is broken or that you have been cheated — it is what a moving market does to an order that asks for “now.” But it is a real cost, and it sits on top of the spread rather than replacing it, so it belongs in the same honest tally.

Putting a number on the spread

A spread quoted in pips is abstract until you convert it into money and into a percentage. Both conversions are worth doing, because a fee expressed one way can only be compared with a fee expressed the same way. The arithmetic is simple and does not need any trading knowledge.

To get the cash cost, multiply the spread (in pips) by what one pip is worth for your trade size. That per-pip value scales with the amount: the bigger the position, the more each pip is worth, so the same spread in pips costs more in cash on a larger trade. Multiply the two together and you have the spread as a figure in your account currency — the same shape as a commission, which is exactly what makes them addable.

To get the percentage, divide that cash cost by the amount you are converting. This is the version that travels furthest, because a percentage compares cleanly against any fee anywhere — a card’s foreign-transaction charge, a transfer provider’s margin, an exchange’s taker fee. A spread that sounds trivial in pips can be a meaningful slice of a small conversion once expressed as a percentage, and a spread that sounds alarming can be a rounding error on a large one. The percentage is what strips away the size and lets you judge the cost on its own terms.

This is the same move at the heart of reading a rate against the midpoint: express the gap as a share of the mid, and the cost stops hiding. If you want to see the arithmetic laid out on a line and compared like-for-like against a headline rate, the companion guide on the mid-market rate and the margin walks through it step by step. Once a spread is a percentage, it stops being jargon and becomes just another number on the bill — one you can line up next to every other cost and rank.

Questions people ask

Is a tighter spread always better for me?

A tighter spread is cheaper to cross, all else equal, so it generally helps. But it’s only one part of the cost — a tight spread paired with a separate commission, or a rate set far from the mid, can still work out dear. Add everything up against the mid-rate before deciding.

Are pips and the spread the same thing?

No. A pip is just the unit prices move in — usually the last decimal place. The spread is measured in pips: a “two-pip spread” means the bid and ask are two of those units apart.

Why did the spread suddenly get wider?

Most often because liquidity thinned or volatility spiked — an exotic pair, a quiet weekend hour, or the moments around a big news release. See market hours and sessions for when trading is busiest.

Does this apply to crypto exchanges too?

Yes. Buying or converting on an exchange has a bid, an ask and a spread, exactly like FX, and sometimes a separate fee on top. The same reading works. If you’re comparing one, check the live numbers on Binance’s own fee page first.

- European Central Bank — euro foreign-exchange reference rates: ecb.europa.eu

- Bank for International Settlements — Triennial Survey of FX market structure and liquidity: bis.org

- European Securities and Markets Authority — investor materials on trading costs: esma.europa.eu

Last updated 6 July 2026. This guide explains how a two-sided quote works and how to compare trading costs; it is not investment, tax or legal advice. Rules and available products differ by country — check your local regulations. Specific spreads, commissions and availability are set by each provider and change constantly — always confirm the live figures on the provider’s own page.

Sign up with the code above for up to 20% off trading fees*. Whatever you decide, confirm the live rates, fees and availability on Binance’s own page first — and never share your password, 2FA code or recovery phrase.

*Up to 20% — you’ll see the exact figure on the Binance sign-up page. This is a sponsored referral link: it won’t cost you more, and the site may earn a commission. See our disclosure.