Most retail FX accounts lose money. Here’s the honest math Who FX trading suits, who it doesn’t, what the broker disclosures say, and how to decide

If you’ve seen an ad promising you can “make income trading forex” and wondered whether it’s real, this guide is for you. It is deliberately sober. It won’t pitch a strategy, a broker or a course, and it won’t tell you that you can’t do it — only what the odds and the disclosures actually say, so you can decide with open eyes. It is not financial advice, and nothing here is a recommendation to trade.

On this page

- Straight to it

- Why the math works against casual traders

- What the broker risk disclosures actually say

- Converting, investing and trading are not the same

- Who FX trading might suit — and who it doesn’t

- Industry red flags to walk away from

- A sober decision checklist

- When to stop

- Where the optimism breaks

- The cost hurdle you clear before any profit

- The part that sinks most beginners isn’t the charts

- What disciplined traders do differently

- If you mainly want currency exposure, not a second job

- Questions people ask

Straight to it

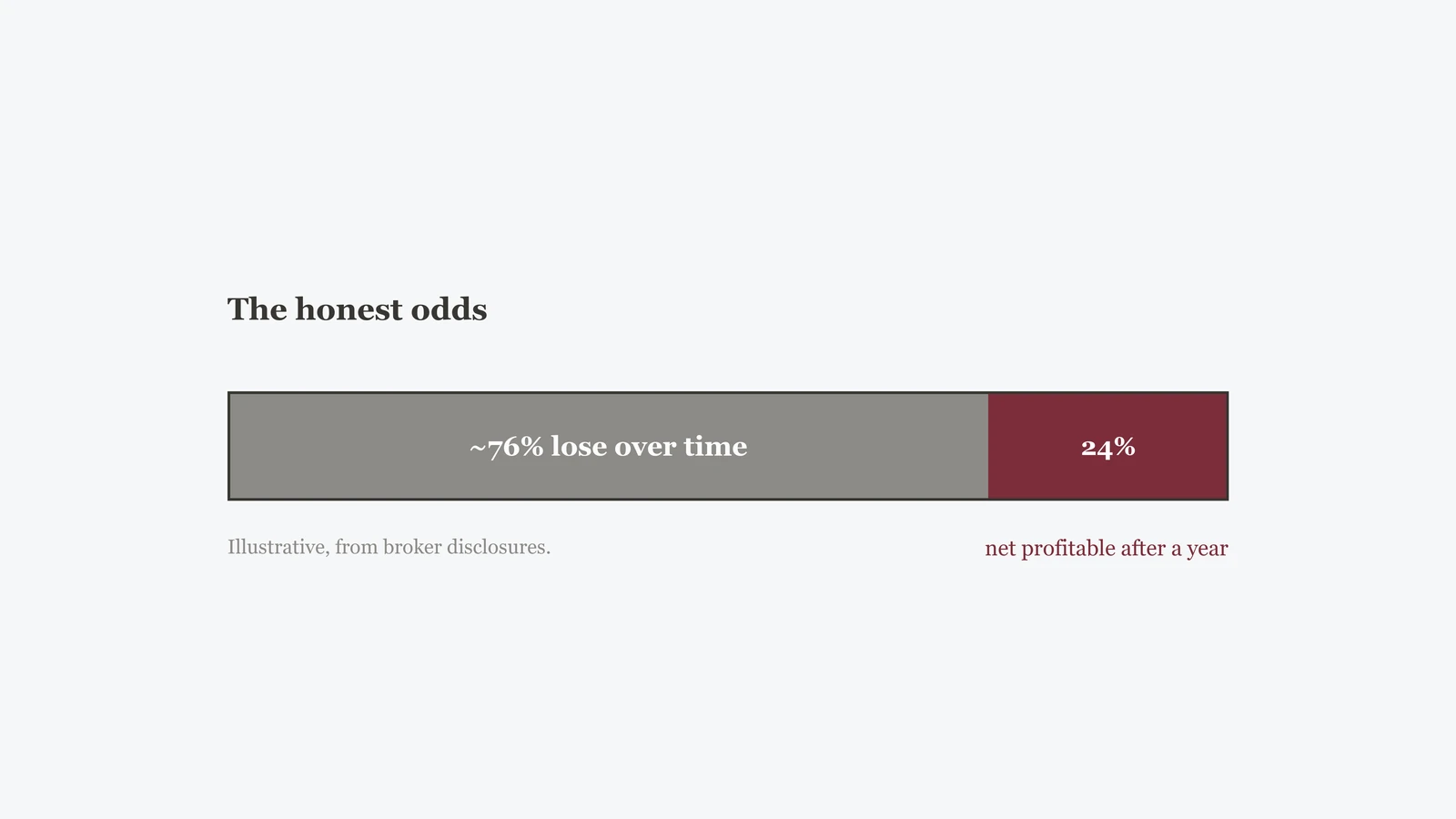

Here is the part the ads leave out: a majority of retail trading accounts lose money over time. This is not a fringe claim — it is documented by financial regulators in several regions, who require brokers to publish exactly that figure. Trading currencies well is a hard, competitive skill that takes years to build, and even then it pays nobody a salary. It is not guaranteed income, and it is the opposite of a steady paycheck. If you go in expecting a reliable monthly return, the math and the data both say you are likely to be disappointed. If you go in treating it as a difficult skill, funded only with money you can fully afford to lose, your eyes are at least open.

Why the math works against casual traders

The currency market doesn’t need to be rigged for most newcomers to lose. Four ordinary forces do the work.

The cost drag on every round trip. Every time you open and close a position, you pay the spread — the small gap between the buy and sell price — and sometimes a commission on top. One round trip barely registers. But an active trader makes hundreds or thousands of round trips a year, and that drag compounds. You have to be right often enough just to cover the cost of playing before you make a single unit of profit. The house, so to speak, takes a sliver of every hand.

Leverage amplifies mistakes. FX brokers offer leverage, which lets a small deposit control a much larger position. That cuts both ways, and it cuts harder on the way down. A move that would be a minor wobble on an unleveraged position can wipe out a leveraged account in minutes. Leverage doesn’t improve your odds of being right; it magnifies the consequences of being wrong. We cover this in depth in leverage and risk.

Emotions are part of the system. Markets move fast, money is on the line, and human beings respond by chasing losses, holding losers too long, cutting winners too early, and over-trading after a bad day. These aren’t character flaws; they are predictable reactions that the structure of trading reliably triggers. They are also the hardest part to fix, because they don’t go away when you read about them.

You’re competing with professionals and algorithms. On the other side of your trade are banks, funds, and automated systems with faster data, lower costs, and full-time research desks. A casual trader on a phone is, in plain terms, the least-informed participant in the room. That doesn’t make winning impossible, but it should reframe what you’re actually up against.

The market doesn’t have to be unfair for most beginners to lose. The cost of every trade, the leverage on the account, and the people on the other side are enough.

What the broker risk disclosures actually say

This is the single most useful thing to know before you open an account, and it’s hidden in plain sight. In many regions, regulators require brokers offering leveraged FX and similar products to publish the percentage of their retail accounts that lose money. You’ll see it as a line near the bottom of a broker’s site or ad — a sentence stating that a large share of retail accounts lose money trading these products with that provider.

The exact percentage varies by broker and over time, so we won’t print a number here — but across these disclosures the figure is consistently a majority. That figure isn’t marketing; it’s a regulatory warning the broker is obliged to show. Reading it as what it is — an official, data-based statement of the odds — is the most honest favour you can do yourself.

When you see “a high percentage of retail accounts lose money trading with this provider,” that is not boilerplate to scroll past. It is the broker telling you, under regulatory obligation, what usually happens to people like you. Take it literally.

Regulators publish plain-language explanations of these risks too. The European Securities and Markets Authority (ESMA) has documented the risks of leveraged FX and contracts-for-difference for retail clients; in the United States, the SEC’s investor education service explains trading risk in plain terms. The roots are listed in the sources below — worth reading before, not after, you decide.

Converting, investing and trading are not the same

A lot of confusion comes from blurring three very different activities. Converting money is a one-time, practical exchange — you need euros for a trip, so you swap dollars for euros. Investing is putting money into assets and holding them for years, accepting ups and downs for long-run growth. Trading is trying to profit from short-term price moves, repeatedly, against other participants. They have different goals, different time horizons and wildly different risk profiles, and a tool that’s sensible for one can be reckless for another.

| Activity | Purpose | Time horizon | Typical risk | Who it’s for |

|---|---|---|---|---|

| Converting | Get the currency you need for a real purpose | Now / one-off | Mainly cost (the margin), not loss of capital | Travellers, freelancers paid abroad, online buyers |

| Investing | Grow money over the long run | Years to decades | Market ups and downs over time | People saving for long-term goals |

| Trading | Profit from short-term price moves | Seconds to weeks | High; most retail accounts lose over time | Few; a skill, not an income source |

If your real need is just to change one currency into another, you don’t need a trading account at all — you need a good rate, which is what the mid-rate and the margin guide is about.

Who FX trading might suit — and who it doesn’t

Trading isn’t for nobody. But the people it might suit look very different from the audience the ads target.

It might suit you if you treat it as a difficult skill rather than an income stream; you fund it only with money you could lose entirely without affecting your life; you set strict, written risk limits before you start and follow them; you keep position sizes small relative to your capital; and you invest in real education and a lot of patient practice, expecting a long apprenticeship with no guarantee at the end. In that frame, the worst case is a contained, affordable loss and the lesson that comes with it.

It does not suit you if you need the money, are counting on it to pay bills or replace a job, or are reaching for emergency savings, rent, or borrowed funds. It does not suit anyone chasing a quick income, anyone who can’t emotionally afford to lose what they put in, or anyone who’s been told it’s a reliable way to earn. If a loss would genuinely hurt your finances or your peace of mind, the honest answer is that this isn’t for you.

Ask: if every unit I put into a trading account vanished tomorrow, would my rent, my bills and my sleep be unaffected? If the answer isn’t a clear yes, the amount is too large — or the activity is the wrong one for you right now.

Industry red flags to walk away from

Around legitimate brokers sits a large ecosystem designed to separate beginners from their money. Treat any of these as a reason to stop:

- Signal sellers and “copy this trade” subscriptions. If someone could reliably predict the market, they wouldn’t be selling tips for a monthly fee.

- Any “guaranteed” claim. Guaranteed profit, guaranteed returns, can’t-lose systems — in trading these are mathematically impossible and a hallmark of a scam.

- Get-rich gurus and lifestyle marketing. Rented cars, beaches and screenshots of profits are sales props, not evidence. The income often comes from selling you a course, not from trading.

- Deposit incentives and pressure to fund fast. Offers that reward you for depositing more, or push you to add money quickly, are nudging you toward the exact behaviour that loses money.

- “Account managers” who trade for you. A stranger who wants your deposit so they can trade on your behalf, often via social media, is a classic fraud setup.

- Anyone implying official backing. No broker, course or signal service is endorsed by a regulator or an exchange because it says so. Verify claims with the regulator directly.

A sober decision checklist

If you’re still weighing it, run honestly through these before you fund anything. Every box should be a genuine yes.

- I have read the broker’s own risk disclosure and noted that a majority of its retail accounts lose money.

- The money I’d use is money I can lose entirely with zero impact on my rent, bills, debts or emergency fund.

- I am treating this as a skill to learn slowly, not a source of income or a way to “make money fast.”

- I have written, specific risk limits — how much per trade, how much in total — and a rule for when I stop.

- I understand how leverage can magnify a loss, and I’ve read the leverage and risk guide.

- The broker is regulated in a recognised jurisdiction, and I’ve checked that directly — not just taken its word.

- I am not relying on signals, “account managers,” or anyone promising guaranteed results.

- I’m emotionally prepared to lose the whole amount and walk away without chasing it back.

If you can’t tick every box, that isn’t a failing — it’s useful information. The most profitable decision many people make about FX trading is not to start.

When to stop

Stop — close the app and step back — the moment you find yourself adding money you can’t afford to lose, trading to win back losses, borrowing or dipping into rent or emergency funds to fund an account, hiding the activity from people close to you, or feeling that you have to trade to feel okay. These are not signs you’re close to a breakthrough; they are signs to stop. If trading is affecting your finances or wellbeing, treat it as a problem to address, not a position to recover.

Where the optimism breaks

The same handful of errors recur, and they’re costly:

- Believing the ad over the disclosure. The headline says “earn income”; the fine print says most accounts lose. Believe the fine print — it’s the part the broker is legally required to mean.

- Confusing a few early wins with skill. Beginners often win at first by luck, then give it all back and more once they size up. Early results prove very little.

- Using money that matters. Rent, savings, borrowed funds — the moment real-life money is in play, fear distorts every decision.

- Treating trading as steady income. Even skilled traders have losing months. Anyone who’s sold it to you as a reliable wage has sold you a fiction.

- Skipping the “could I lose it all?” question. If you haven’t honestly answered it, you haven’t made a decision — you’ve made a wish.

The cost hurdle you clear before any profit

The earlier section on the math mentioned the spread in passing. It’s worth slowing down on, because it changes how you should read every “I’m up 3% this week” story you hear. On a leveraged FX position, you don’t start at zero and hope to climb. You start slightly below zero, and you have to climb back to break even before a single unit of profit is yours.

Three costs put you there. The spread is the gap between the price you buy at and the price you could sell at the same instant; the moment you open, that gap is already against you. A commission, if your broker charges one instead of or alongside a wider spread, is a second bite. And if you hold a position overnight, there’s usually an overnight financing charge — often called a swap or rollover — because leverage means you’re effectively borrowing to hold the position, and borrowing has a cost. None of these is dramatic on its own. That’s exactly why they’re easy to underestimate.

The problem is repetition. A single round trip barely moves the needle, but costs don’t care whether a trade won or lost — they apply either way, every time. Run hundreds or thousands of trades a year, add overnight charges on anything you hold, and the drag compounds into a real headwind that sits on top of the market risk you already took. To come out ahead over time, you don’t just need to be right more often than wrong. You need an edge that’s reliable enough to cover all of that friction and then pay you — a genuinely repeatable advantage over the other participants. Most people never find one, and there’s no shame in that; it’s a demanding bar. The figures above are illustrative of how the costs stack, not a formula that turns into profit.

Every position opens at a small loss because of the spread, and holding it overnight can add a financing charge. Those costs repeat on every trade, win or lose. Clearing them consistently — before you make anything — is what a real trading edge has to do, and most people don’t have one.

The part that sinks most beginners isn’t the charts

Newcomers tend to assume the hard part is reading the market — the indicators, the patterns, the setups. In practice, the charts are rarely what does the damage. What does the damage is ordinary human wiring under pressure, and it shows up the same way in most people.

Loss aversion makes a loss feel worse than an equal gain feels good, so a losing position is genuinely painful to close. That’s where chasing losses starts: rather than take the small, planned loss, people hold on hoping it comes back, or open a bigger trade to win it back faster — which is how a manageable loss becomes an account-sized one. After a bad run, over-trading creeps in, taking trades out of frustration or boredom rather than any real signal, each one carrying the costs from the section above. And when a trade goes against them, some quietly move the stop-loss further away, converting a defined risk into an open-ended one because admitting the trade was wrong hurts more than the growing loss does — until it doesn’t.

These aren’t signs of a weak or foolish person. They’re common patterns that the structure of trading reliably pulls out of ordinary people, and reading about them — here or anywhere — doesn’t switch them off. A course won’t either; the emotions still arrive when real money is moving. That’s worth knowing before you start, because it means the honest question isn’t “can I learn to read a chart” but “can I sit calmly through the part where my own instincts work against me.” Many capable people find, fairly, that they’d rather not.

What disciplined traders do differently

The small minority who last don’t have a secret indicator. What tends to separate them is boring, unglamorous process — the opposite of what the ads sell. It’s worth describing plainly, not as a promise that copying it makes trading work, but so you can see how much structure the durable few impose on themselves.

- Fixed risk per trade. They decide in advance how small a share of their capital any single trade can lose — and keep it small — so no one trade, and no bad run of them, can do outsized damage. The position size follows from that limit, not from how confident they feel.

- A written plan. Before a trade, they’ve defined what would make them enter, where they’d exit if they’re wrong, and where they’d take profit if they’re right — on paper, not in their head, where it can quietly move mid-trade.

- A trading journal. They record trades and, more importantly, the reasoning and the emotion behind them, then review it. It’s how a person catches their own recurring mistakes instead of repeating them with more money.

- They treat it as a business with a budget they can lose. The capital is a defined, walled-off amount they’ve accepted they might lose entirely — never rent, savings or borrowed money — and they measure results over long stretches, expecting losing days and losing months as a normal cost of the activity.

Notice that none of this is about predicting the market better. It’s about controlling losses, removing in-the-moment decisions, and staying solvent and level-headed long enough to learn. It’s also demanding to sustain, which is part of why the durable group stays small. Doing all of it improves how you handle risk; it does not guarantee a profit, and no honest description of it would say otherwise.

If you mainly want currency exposure, not a second job

It’s worth separating two very different wishes that often get bundled together. One is wanting to trade — to actively profit from short-term moves, which is the demanding, time-hungry activity this whole guide is about. The other is simply wanting some exposure to a currency, or to worry less about the currency you already hold. Those don’t require the same thing, and confusing them is how people end up with a trading account they never really wanted.

If the real goal is exposure rather than a second job, there are lower-effort ways people think about it, and the honest first step is to get clear on the goal before reaching for any of them. If you’ll spend money in another currency — a trip, a payment, a purchase — then simply holding some of that currency ahead of time, through an ordinary account, covers the need without any trading at all. If the goal is broad, long-term growth rather than a currency bet specifically, some people prefer low-cost, diversified funds held for years, where currency is one small ingredient among many rather than the whole position. And for a great many people, the most honest answer is that they don’t actually need dedicated FX exposure at all — the question dissolves once they name what they were really trying to achieve.

None of that is a recommendation of any specific product, and none of it is advice; the right path depends entirely on your own goals, circumstances and tax situation, which is a conversation for a qualified, independent professional, not a web page. The point is narrower and it’s this: if you don’t genuinely want the work, the risk and the losing months that trading involves, don’t back into them because “forex” was the first word you reached for. Start from the goal. If it turns out to be conversion, the conversion checklist is the practical next stop, and the mid-rate and the margin guide explains what a fair rate looks like.

Questions people ask

Can anyone actually make money trading forex?

A minority of people do trade profitably over the long run, usually after years of work, strict discipline and real capital. But the broker disclosures are clear that they are the minority. Plan for the documented outcome, not the exception.

Is forex trading a scam?

The market itself is real and the regulated brokers are legitimate businesses. The scams sit around it — signal sellers, “account managers,” guaranteed-profit courses and get-rich gurus. The activity is legal and risky; much of the marketing around it is the part to distrust.

How is FX trading different from buying crypto?

Both involve price risk, spreads and the same emotional traps, but the markets, hours and instruments differ. If you’re comparing the always-on crypto market, read FX vs the crypto market for an even-handed look.

Should I just convert currency instead?

If your real need is to change money for a trip, a payment or an online purchase, then yes — you need a good conversion, not a trading account. Start with the conversion checklist.

- European Securities and Markets Authority — investor protection and product-intervention work on leveraged FX/CFDs: esma.europa.eu

- U.S. Securities and Exchange Commission — investor education on trading risk: investor.gov

- U.S. Securities and Exchange Commission — main regulator site: sec.gov

- OECD — financial consumer protection and literacy: oecd.org

Last updated 6 July 2026. This guide explains risk and how to think about the decision; it is not investment, tax or legal advice, and it is not a recommendation to trade. The “majority lose” point reflects figures regulators require brokers to publish; exact percentages vary by provider and over time, and any numbers here are illustrative, not a quote. Rules and protections are country-specific — check your local regulator and the broker’s own disclosures.

This guide won’t tell you to trade — most retail accounts lose money, and that’s the honest headline. But if you’ve read it straight and still want to try, with money you can afford to lose, the code above gets you up to 20% off trading fees* when you open a Binance account. It costs you nothing extra. Confirm the live rates and rules on Binance’s own page first, and never share your password, 2FA code or recovery phrase.

*Up to 20% — you’ll see the exact figure on the Binance sign-up page. This is a sponsored referral link: it won’t cost you more, and the site may earn a commission. See our disclosure.