Getting paid to hold a currency — until you’re not The carry trade, interest-rate differentials and swap, and why “free yield” reverses

You’ve probably read the pitch: hold the right currency and you earn interest just for sitting still. It sounds like money for nothing. There is a real mechanism underneath it — the carry trade — but there is also a catch that the pitch tends to skip. This guide explains what the carry trade is, where the interest actually comes from, and why a quiet stream of yield can reverse into a sharp loss in a matter of days. It explains a concept; it is not a recommendation to do it, and it won’t tell you which way any currency is headed.

On this page

- The catch, up front

- Why two currencies pay different rates

- What the carry trade actually is

- Swap and rollover: the daily ledger

- The renting-cheap-money analogy

- Why it can work in calm markets

- The catch: when carry reverses

- How leverage magnifies both sides

- It is not free yield

- Where carry traders slip

- Questions people ask

The catch, up front

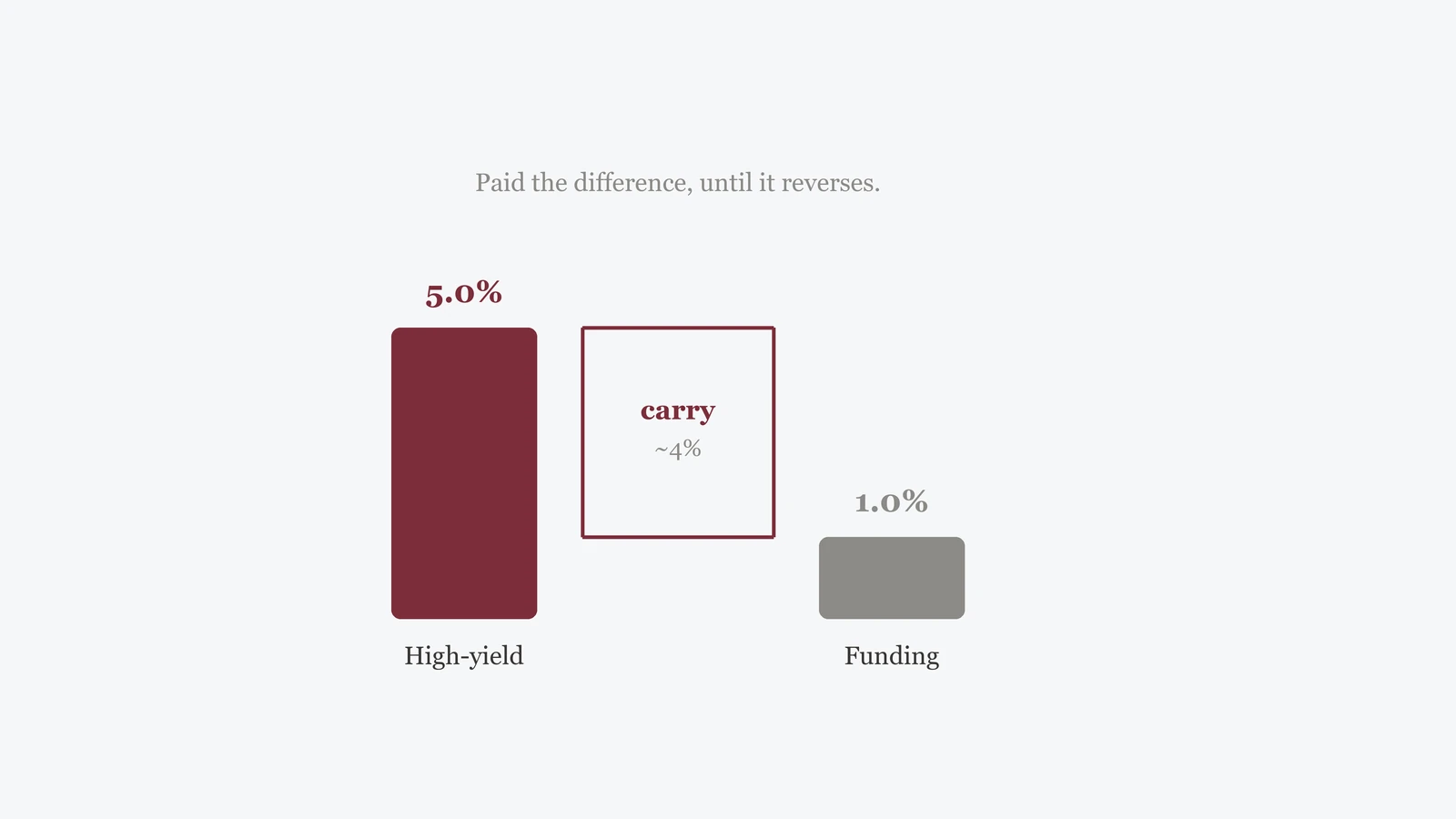

The carry trade means holding a higher-yielding currency funded by a lower-yielding one, and pocketing the difference in interest rates — the interest-rate differential. In a brokerage position you see this as swap (or rollover): a small amount paid or received each time you hold the position overnight. When markets are calm and the funding currency stays put, the differential trickles in. The trouble is that the same position carries currency risk: if the higher-yielding currency falls against the funding currency, the move can wipe out months of accumulated interest in days. It is a real strategy, not free yield, and it has a long history of sudden reversals.

Why two currencies pay different rates

The interest-rate differential is simply the gap between the short-term interest rates of two currencies — how much more one pays to hold than the other. Every currency is tied to a short-term interest rate set, broadly, by its central bank. Those rates are not the same everywhere, because each economy faces different inflation, growth and policy conditions. A central bank fighting high inflation may hold rates well above one that is trying to encourage borrowing. The gap between two countries’ short-term rates is the interest-rate differential, and it is the engine of the carry trade.

Because money in the wholesale market can be borrowed in one currency and lent in another, that differential becomes tradable. If one currency’s short rate is meaningfully higher than another’s, a position that is long the higher-yielding one and short the lower-yielding one earns roughly that difference over time — before any currency movement is taken into account. The two pieces, the yield you collect and the exchange-rate move you’re exposed to, are separate, and keeping them separate in your head is the whole point of this guide.

What the carry trade actually is

A carry trade is a position built to harvest that differential. You hold a higher-yielding currency and fund it by being short a lower-yielding one — the so-called funding currency. As long as the position stays open and the differential stays positive in your favour, you accrue the gap. Historically, traders have used low-rate currencies as the funding leg and rotated into whichever higher-rate currency offered the widest spread.

The crucial thing to notice is that you are not just earning interest. You are also holding an open currency position, which means you are exposed to where the exchange rate goes. The interest is the part people advertise. The exchange-rate exposure is the part that decides whether the trade actually made money.

Swap and rollover: the daily ledger

On a brokerage platform you rarely see the words “interest-rate differential.” You see swap, sometimes called rollover or overnight financing. Each day a position is held past the platform’s daily cut-off, the broker credits or debits a small amount that reflects the rate difference between the two currencies in your pair, plus the broker’s own markup.

- Positive swap: if you’re long the higher-yielding currency, you may receive a small amount each night.

- Negative swap: if you’re positioned the other way, you pay each night — and the same overnight cost works against you.

- Broker markup: the swap you actually get is not the raw differential. The platform usually keeps a slice, so the real number is smaller than the headline rate gap.

- Triple swap days: many platforms charge or credit several days’ worth on one weekday to account for the weekend, so the daily figure is not uniform.

Swap is where the carry trade meets your account statement. It is also where a position can quietly bleed if you’re on the wrong side of the differential, or if the broker’s markup turns a thin positive swap into a negative one.

The renting-cheap-money analogy

Here is a currency-native way to picture it. Think of borrowing one currency cheaply — renting money where rent is low — and parking that money in another currency where it earns a higher rate. While the two rents stay where they are, you keep the spread between what you pay to borrow and what you earn to hold. That spread is the carry.

The carry is the rent you collect for holding the position. The exchange rate is the value of the thing you’re holding — and that value can fall faster than any rent comes in.

The analogy also makes the danger obvious. You are still holding an asset whose price moves. If the currency you parked your money in loses value against the one you borrowed, the drop in price can dwarf every cent of rent you collected. The rent is steady and small; the price move can be sudden and large.

Why it can work in calm markets

Carry tends to behave best in quiet conditions: stable interest-rate expectations, low volatility, and no scramble for safety. In those stretches, exchange rates can drift sideways or even move gently in the carry trader’s favour, so the differential accumulates with little drama. This is why carry has periods where it looks almost serene — a slow, repeatable trickle.

That calm is exactly what makes it seductive, and exactly what makes it dangerous. A long run of uneventful days lulls people into treating the yield as dependable and the currency risk as theoretical. The history of currency markets is full of stretches where carry worked smoothly for a long time and then unwound violently in a short one.

The catch: when carry reverses

The defining feature of the carry trade is asymmetry. The interest comes in slowly; the loss can arrive all at once. When markets turn “risk-off” — a shock, a policy surprise, a rush toward safer assets — crowded carry positions get unwound together. Everyone reaches for the exit in the same direction at the same time, the higher-yielding currency drops sharply against the funding currency, and the move can erase months of accumulated carry in a few days.

Here is an illustrative picture of that asymmetry over a holding period. These are made-up numbers to show the shape of the risk, not a forecast or a quote:

| Over the period (illustrative) | What carry pays | What an adverse FX move can cost |

|---|---|---|

| 3 months of calm, differential accruing | +1.5% | 0% |

| One risk-off week, higher-yielder falls 4% | +0.1% | −4% |

| Net result for the period | +1.6% earned | −4% lost |

The differential paid out for months; a single bad week more than reversed it. Illustrative, not a quote — the point is the shape, not the figures. This is the pattern carry has shown repeatedly: long, quiet accrual punctuated by short, sharp reversals.

Your total result is the carry you collect plus or minus the exchange-rate move — never the carry alone. Any pitch that quotes the yield without the currency exposure is showing you half the position.

How leverage magnifies both sides

Carry trades are often run with leverage, because the raw differential on an unleveraged position can look small. Leverage scales the position up, which scales the swap you receive — and scales the loss from an adverse move by exactly the same multiple. A 4% drop on a position leveraged several times over is no longer a 4% dent; it can be a large fraction of your account, and it can trigger a margin call that closes the position at the worst possible moment.

This is the part that turns a slow strategy into a fast wipe-out. The yield grows linearly with leverage, but so does the downside, and the downside arrives suddenly. If you don’t already understand how borrowed exposure amplifies outcomes, read leverage and risk in forex before you go anywhere near a leveraged carry position.

Step back if any of these are true: someone presents the carry yield as dependable income without mentioning currency risk; an account or “programme” promises a set return for holding a currency; you’re using leverage you couldn’t cover if the position moved several percent against you overnight; you can’t see the actual swap your broker pays after its markup; or anyone pressures you to fund a position fast to “lock in” a rate. A steady yield with an unbounded, sudden downside is not a safe income stream.

It is not free yield

The honest framing is this: the carry trade pays you a real interest-rate differential, and in exchange you carry a real currency risk that can reverse the whole thing quickly. The yield is not a reward for nothing — it is, in part, compensation for bearing exactly the risk that occasionally shows up all at once. “You earn interest just for holding” is true on the days nothing happens, and badly incomplete on the day something does.

None of this means carry is a trick. It means the interest and the exchange-rate exposure are two halves of one position, and you only understand the trade when you hold both halves in view at the same time.

Where carry traders slip

The errors that hurt people most with carry are predictable:

- Counting the yield, ignoring the currency. Treating swap as income while forgetting you’re holding an open exchange-rate position is the classic mistake. Always net the two together.

- Mistaking a calm streak for safety. A long quiet period is not evidence the risk is gone; crowded carry tends to unwind precisely when everyone feels safest.

- Over-leveraging the differential. Because the raw carry is small, people lever it up — and turn a manageable currency move into an account-ending one.

- Forgetting the broker’s markup. The swap you actually receive is smaller than the headline rate gap; sometimes it’s negative once the markup is applied.

Questions people ask

Do I really earn interest just for holding a currency?

You earn (or pay) a swap based on the interest-rate differential between the two currencies in your pair, less your broker’s markup. But you are also holding an open exchange-rate position, so the swap is only half the story — the currency move is the other half.

Why does the carry sometimes reverse so fast?

Carry positions tend to be crowded, and they share a common risk. When markets turn risk-off, many people unwind at once, the higher-yielding currency drops sharply, and a few days can undo months of accrued interest. The forces behind those moves are covered in what moves an exchange rate.

Does leverage make the carry trade safer or riskier?

Riskier. Leverage scales the swap you receive and the loss from an adverse move by the same multiple, and it can force the position closed via a margin call. See leverage and risk.

Is the carry trade something I should do?

This guide explains the concept, not whether it suits you — that depends on your situation and the local rules where you are. Treat any “steady yield” framing with caution, and read the risk material before committing real money.

- Bank for International Settlements — research on carry trades and FX market structure: bis.org

- International Monetary Fund — interest rates, capital flows and exchange-rate concepts: imf.org

- European Central Bank — monetary policy and short-term interest rates: ecb.europa.eu

- Federal Reserve — policy rate background and explainers: federalreserve.gov

Last updated 6 July 2026. This guide explains the carry trade and interest-rate concepts; it is not investment, tax or legal advice. Interest rates, swap and exchange rates change constantly, and rules differ by country — always confirm the live figures and your local rules before acting.

Sign up with the code above for up to 20% off trading fees*. Whatever you decide, confirm the live rates, fees and availability on Binance’s own page first — and never share your password, 2FA code or recovery phrase.

*Up to 20% — you’ll see the exact figure on the Binance sign-up page. This is a sponsored referral link: it won’t cost you more, and the site may earn a commission. See our disclosure.