Why a currency you’ve never traded can change your grocery bill What an exchange rate is, and the real forces that move it — interest rates, inflation, trade and sentiment

A headline says a far-off central bank raised interest rates, and a few weeks later your imported coffee, your streaming subscription and your next holiday all cost a little more. The link is the exchange rate. This guide is for anyone curious about why rates move and how that movement reaches everyday life. It is not a forecast, a trading signal, or a promise about where any currency is headed — if anything, one of its main jobs is to explain why no honest guide can give you that.

On this page

- The one-paragraph version

- What an exchange rate actually is

- Supply and demand: the engine underneath

- Force one: interest rates and central banks

- Force two: inflation and purchasing power

- Force three: trade balances and capital flows

- Force four: sentiment, risk-on and expectations

- How the forces pull against each other

- Floating, pegged and managed currencies

- Why you can’t reliably predict rates

- How a rate move reaches your everyday life

- Where people go wrong

- How to follow a rate sensibly

- Questions people ask

The one-paragraph version

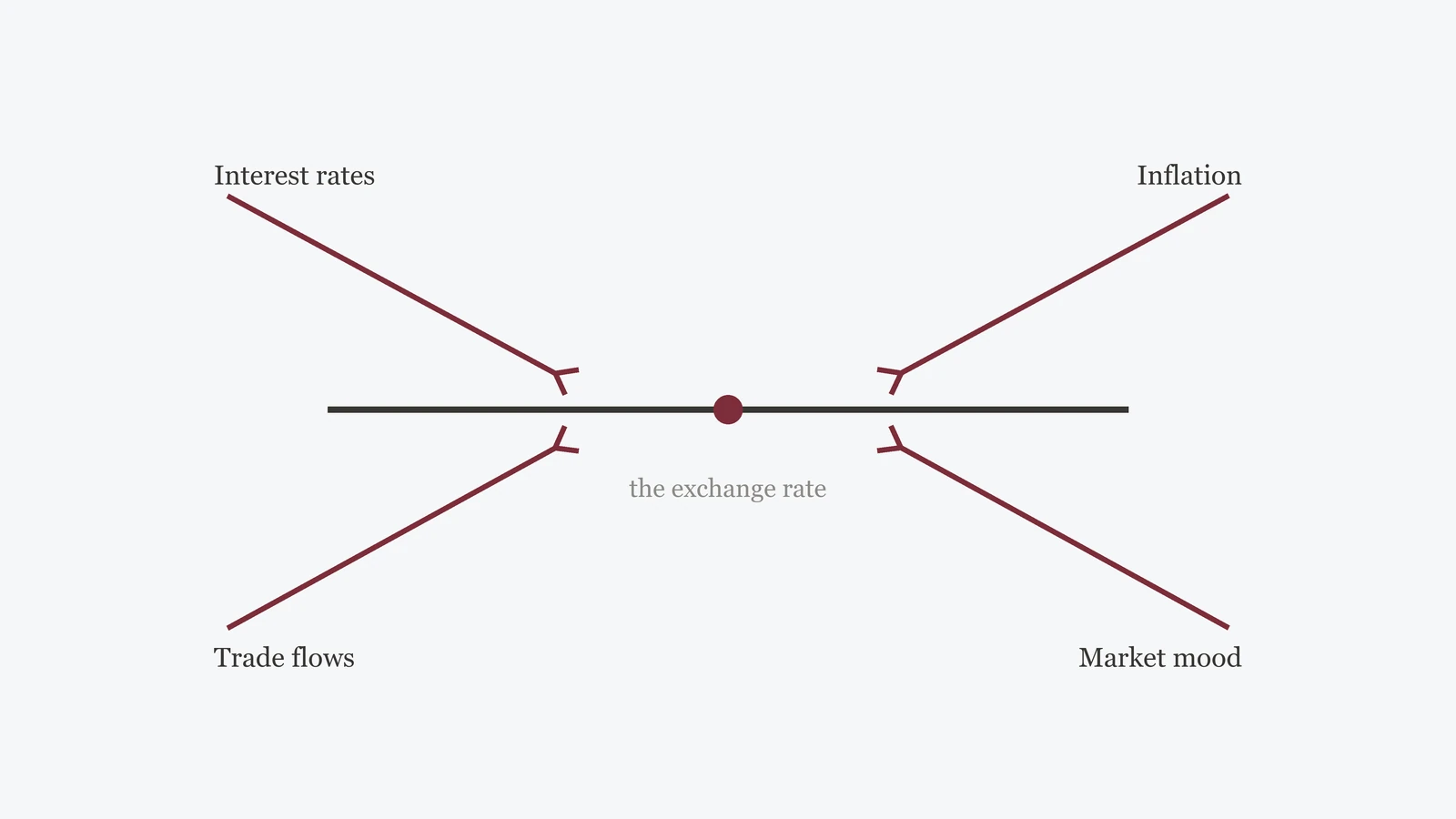

An exchange rate is simply the price of one money measured in another, and like any price it moves when supply and demand shift. Four big forces do most of the pushing: interest rates set by central banks, inflation and purchasing power, trade and investment flows, and market sentiment about risk and the future. They constantly pull against one another, which is exactly why no one can reliably predict where a rate will go next. Understanding the forces helps you read the news calmly — not call the market.

What an exchange rate actually is

An exchange rate is the relative price of one currency in terms of another. When you read that one euro is worth 1.08 US dollars, that figure is doing the same job as the price tag on any product: it tells you how much of one thing you must give up to get a unit of another. The twist with money is that both sides are themselves prices, so the number describes a relationship rather than a single object. A rate going up for one currency is, by definition, a rate going down for the other.

Because it’s a relationship, an exchange rate never moves “on its own.” It moves when the balance between people wanting to buy a currency and people wanting to sell it changes — the same wholesale-versus-retail logic you see anywhere. The mid-market price quoted on a news ticker is the wholesale, interbank reference; what an airport bureau offers you is the retail version with a margin added. If that distinction is new, our guide on the mid-rate and the margin unpacks it. For now, hold one idea: a rate is a price, and prices respond to demand.

Supply and demand: the engine underneath

Every force described below is really just a different reason for someone to buy or sell a currency. That is worth saying plainly, because the financial press tends to present interest rates, trade figures and investor mood as separate machines. They aren’t. They are all channels through which demand for one money rises or falls relative to another.

When more people want to hold a currency — to invest there, to buy that country’s goods, to park money somewhere they trust — demand rises and, all else equal, the currency strengthens. When holders want out, supply rises and it weakens. “All else equal” is the catch: in real markets, several forces move at once and partly cancel. Keep the engine in mind and the four forces stop looking like magic and start looking like reasons to trade.

A currency strengthens when more people want to hold it than to let it go. Every force below is just a reason behind that wanting.

Force one: interest rates and central banks

Of the four forces, interest rates get the most airtime, and for good reason. A central bank — the institution that sets a country’s benchmark interest rate — influences how much return a saver or investor can earn by holding money in that currency. When a central bank raises its rate, assets denominated in that currency tend to pay more, which can attract money from abroad. More inbound demand for the currency, all else equal, tends to push it stronger.

Lower rates work the other way: the currency becomes a less rewarding place to park money, and some of that money looks elsewhere. But the relationship is far from mechanical. Markets are forward-looking, so what often matters is not today’s rate but how it compares to what investors already expected. A rate rise that everyone anticipated may move a currency very little, while a surprise — or a hint about future moves — can move it sharply. Central banks also publish minutes, forecasts and speeches, and traders parse every word for clues. This anticipation game is why a currency can fall on good news, if the news was simply less good than the market had already priced in.

A “central bank” is the public institution responsible for a currency — setting benchmark interest rates and aiming for stable prices. Examples include the European Central Bank, the US Federal Reserve and the Bank of England. They influence rates; they do not hand out guaranteed outcomes.

Force two: inflation and purchasing power

Inflation is the rate at which a currency loses purchasing power — how quickly the same money buys less over time. It connects to exchange rates through a simple idea: a currency that is losing value at home tends, over the long run, to lose value against currencies that are holding theirs better. If prices in one country are rising much faster than in another, a unit of the high-inflation currency buys progressively fewer goods, and markets gradually re-price it lower against the steadier one.

This long-run pull is sometimes described as currencies drifting toward levels where a basket of goods costs roughly the same across borders. It is a tendency, not a timetable. Over months and years it can be swamped by interest rates and sentiment; over a decade it tends to reassert itself. Inflation also loops back into the first force, because central banks raise interest rates partly to cool inflation — so a single inflation report can move a currency twice, once through purchasing power and once through what it implies about the next rate decision.

Force three: trade balances and capital flows

Currencies are needed to pay for things across borders, so the pattern of trade and investment matters. When a country exports more than it imports, foreign buyers must acquire its currency to pay for those exports, which is a source of demand. When it imports more than it exports, the flow runs the other way. The trade balance — exports minus imports — is one input into how much of a currency the world needs at a given moment.

In modern markets, though, capital flows often dwarf trade flows. Money moving to buy shares, bonds, property or whole businesses in another country can shift a currency far faster than the slow grind of import and export invoices. A wave of foreign investment into a country’s assets lifts demand for its currency; a sudden exit does the reverse. This is why a currency can strengthen even when the trade balance looks poor: investors may be piling into its assets for reasons that have nothing to do with the goods crossing its borders.

| Force | Pushes the currency stronger when… | Pushes it weaker when… |

|---|---|---|

| Interest rates | rates rise (or surprise higher) versus other countries, drawing money in | rates fall or lag, making the currency a less rewarding place to hold money |

| Inflation | inflation stays low and stable relative to others, protecting purchasing power | inflation runs high, eroding what the currency buys over time |

| Trade & capital flows | exports and inbound investment create demand for the currency | heavy imports or an investor exit reduce demand for it |

| Sentiment / risk | it’s seen as a safe place to sit during stress, attracting nervous money | risk appetite returns or confidence in it drops, sending money elsewhere |

The directions above are general tendencies, not rules. In practice the forces overlap, and the table is a way to organise your thinking — not a predictor.

Force four: sentiment, risk-on and expectations

The first three forces are grounded in fundamentals you can measure. The fourth is mood, and it can dominate everything else in the short term. Markets swing between “risk-on” phases, when investors feel confident and chase higher returns, and “risk-off” phases, when fear takes over and money rushes toward whatever feels safest. During risk-off episodes, certain currencies have historically attracted nervous money simply because they’re seen as stable stores of value, and they can strengthen even when their own fundamentals haven’t changed at all.

Sentiment is powered by expectations, and expectations react to news, rumour, politics and crises long before any official figure confirms them. An election result, a geopolitical shock or a single alarming headline can move a currency in minutes. This is also the force most vulnerable to herd behaviour and overshooting: a move that starts with a real reason can run far past it as traders pile in, then snap back. Because mood is so hard to measure and so quick to reverse, it’s the single biggest reason short-term rate moves resist prediction.

How the forces pull against each other

If the four forces always pointed the same way, currencies would be easy to read. They rarely do. A country might raise interest rates — a strengthening force — precisely because its inflation is high, which is a weakening force. Strong export demand might coincide with investors fleeing its assets over political worries. At any given moment a currency is the net result of several tugs in different directions, and the “winner” can change week to week.

This tug-of-war is why headlines so often seem contradictory. One day a rate rises on interest-rate news; the next it falls on a risk-off wobble, with the underlying economy unchanged. There is no fixed ranking that says interest rates always beat sentiment, or trade always beats inflation. Which force leads depends on what the market is most focused on right then — and that focus itself shifts. Holding all four in view at once, rather than latching onto one, is the closest thing to an accurate mental model.

Floating, pegged and managed currencies

Not every currency floats freely. In a floating regime — which covers most major currencies — the rate is set by the market, moving continuously as the forces above play out. In a pegged regime, a government or central bank commits to holding its currency at or near a fixed value against another currency (or a basket), and intervenes to defend that level. Many currencies sit somewhere in between, in a managed float where authorities mostly let the market lead but step in during turbulence.

The regime changes which forces matter most. A free float responds to all four pressures in real time. A peg can look unnervingly stable for years — until the cost of defending it becomes too high and it shifts or breaks, sometimes abruptly. Whether a particular currency is floating, pegged or managed depends on each country’s own policy choices, and those can change; if you need the current arrangement for a specific currency, check a qualified, up-to-date source rather than assuming.

Why you can’t reliably predict rates

Here is the honest part. Everything above explains why rates move, but explanation after the fact is very different from prediction before it. Several things conspire against forecasting. The forces pull in different directions, so even knowing all of them doesn’t tell you which will win. Markets are forward-looking, so today’s known facts are often already baked into the price — what moves the rate is the surprise, and surprises are by definition unpredictable. And sentiment can override fundamentals for long, irrational stretches.

This is why even large institutions with enormous resources are routinely wrong about currencies, and why short-term FX forecasting has a famously poor track record. It is not a skill gap you can close with the right course or signal service. Anyone who claims to know where a rate is heading — especially anyone selling that claim — is either guessing or selling. The useful goal isn’t to predict the next move; it’s to understand the forces well enough to read events without panic and to recognise a sales pitch when you see one.

Be very wary of anyone who promises to predict exchange rates, sells “signals” or forecasts, claims a method that “can’t lose,” or pressures you to act on a tip before a deadline. No legitimate source can tell you where a rate will go. Treat confident predictions, paid signal groups and urgency tactics as warnings, not opportunities.

How a rate move reaches your everyday life

You don’t have to trade currencies to feel them. When your home currency weakens against another, anything priced in that other currency gets more expensive for you — and a surprising share of everyday spending is priced abroad somewhere up the chain.

- Imported goods. Electronics, clothing, coffee, cars and countless components are made or sourced abroad. A weaker home currency raises their landed cost, and some of that reaches the shelf price.

- Fuel and energy. Oil and gas are traded internationally and often priced in US dollars. If your currency weakens against the dollar, the same barrel costs you more, which can ripple into transport and heating bills.

- Travel. The most direct hit. A weaker home currency means your money buys less abroad — hotels, meals and transport all feel pricier, even if local prices haven’t changed at all.

- Online subscriptions priced overseas. Streaming, software and app-store charges billed in another currency rise and fall with the rate, so a foreign-priced subscription can quietly creep up on your statement.

None of this happens instantly or in lock-step — businesses hedge, absorb costs and adjust prices on their own schedules — but over time, a sustained rate move tends to show up in what you pay. That’s the quiet thread connecting a distant policy decision to your weekly shop.

Where people go wrong

A few misunderstandings trip people up again and again:

- Treating one force as the whole story. “Rates went up, so the currency must rise” ignores the other three forces that may be pulling the other way. The net result is what shows up on the screen.

- Confusing explanation with prediction. Understanding why a rate moved yesterday gives you no reliable edge on tomorrow. The past is legible; the future isn’t.

- Mistaking a strong currency for a strong economy. They’re related but not the same. A currency can rise on risk-off flows even as the economy struggles, and a healthy economy can run a deliberately weaker currency.

- Reacting to every wiggle. Rates jitter constantly. For most real-life decisions, the broad trend over weeks matters far more than the noise of a single day.

- Believing someone can call the move. If forecasting worked, the people selling forecasts wouldn’t need to sell them. Confident predictions are a red flag, not a service.

How to follow a rate sensibly

If a particular rate matters to you — for a trip, a transfer, a foreign subscription — here’s a calm way to keep an eye on it without falling for noise or sales pitches.

- Identify the exact pair you care about (for example, your home currency against the one you’ll be spending), and find its current mid-market rate from a neutral source.

- Look at the trend over the past few months, not just today’s number. One day’s move is mostly noise; the direction over weeks is the signal that affects your costs.

- When you read news that moves the rate, ask which of the four forces it touches — interest rates, inflation, trade and flows, or sentiment — and remember the others may be pulling back.

- Resist the urge to act on any single forecast or “tip.” Treat predictions as opinion, never as fact, and ignore anyone selling certainty.

- When you do need to convert, judge the offer against the mid-rate rather than the trend — the margin you’re charged is something you can control, unlike the rate itself.

Any specific figure in this guide is illustrative, not a quote. Live rates change every second and vary by provider — always read the current number on a neutral source or the provider’s own screen before you decide anything.

Questions people ask

Which force matters most for a currency?

It depends, and that’s the honest answer. Over short periods, sentiment and interest-rate surprises often dominate; over years, inflation and purchasing power tend to reassert themselves. There’s no fixed ranking — which force leads shifts with whatever the market is focused on at the time.

If interest rates rise, does the currency always go up?

No. Higher rates can attract money and strengthen a currency, but only if the rise surprises the market and isn’t outweighed by high inflation, weak confidence or an investor exit. Plenty of rate rises are met with a flat or falling currency because they were already expected.

Can anyone reliably predict where a rate is going?

No one can do it reliably — not banks, not funds, not signal sellers. The forces conflict, surprises drive the moves, and mood can override the rest. Anyone promising to predict rates, or selling forecasts and signals, should be treated as a warning sign rather than a guide.

How does a foreign rate affect prices where I live?

Through imported goods, internationally priced fuel and energy, travel costs and any subscriptions billed in another currency. When your home currency weakens, those tend to cost more over time, though the effect is gradual and depends on local conditions. For anything country-specific, check a qualified local source.

- European Central Bank — monetary policy and euro reference rates: ecb.europa.eu

- US Federal Reserve — monetary policy and interest rates: federalreserve.gov

- Bank for International Settlements — FX market structure and research: bis.org

- International Monetary Fund — exchange-rate concepts and data: imf.org

Last updated 6 July 2026. This guide explains how exchange rates move and why they resist prediction; it is not investment, tax or legal advice. Specific figures are illustrative, not quotes, and rules differ by country — for anything country-specific, check a qualified local source, and always confirm live figures on the provider’s own page.

Sign up with the code above for up to 20% off trading fees*. Whatever you decide, confirm the live rates, fees and availability on Binance’s own page first — and never share your password, 2FA code or recovery phrase.

*Up to 20% — you’ll see the exact figure on the Binance sign-up page. This is a sponsored referral link: it won’t cost you more, and the site may earn a commission. See our disclosure.