Why some currencies barely move and others swing daily Fixed, floating and pegged exchange rates — how each is set, and why it matters when you convert or travel

Look up two currencies and you’ll notice something odd: one drifts a fraction of a percent a day, another sits at what looks like exactly the same number month after month. That difference isn’t chance — it’s the exchange-rate regime a country has chosen. This guide explains the two ends of the spectrum, floating and fixed, plus the managed middle and the currency peg that sits between them. It’s plain-English background, not a forecast: nothing here predicts where any rate is going.

On this page

- Quick version

- Floating rates: the market decides

- Fixed rates and how a peg is held

- The managed float in between

- Types of peg: hard, crawling, band

- What a peg break means for people

- Why this matters when you convert or travel

- How a peg is actually defended

- Currency boards and dollarization

- Why a country picks one regime over another

- Questions people ask

Quick version

An exchange rate is either left to the market, held by the authorities, or something in between. A floating rate is set by supply and demand and moves continuously — sometimes a lot. A fixed or pegged rate is held at, or close to, a chosen value by a central bank that trades its own currency against foreign reserves to keep it there. A managed float mostly lets the market lead but allows the central bank to lean against big swings. Pegs come in flavours — hard, crawling, or a band the rate is allowed to wander within — and when a country can no longer hold a peg, the rate can move fast. Knowing which regime a currency runs on explains why it behaves the way it does when you go to change money.

Floating rates: the market decides

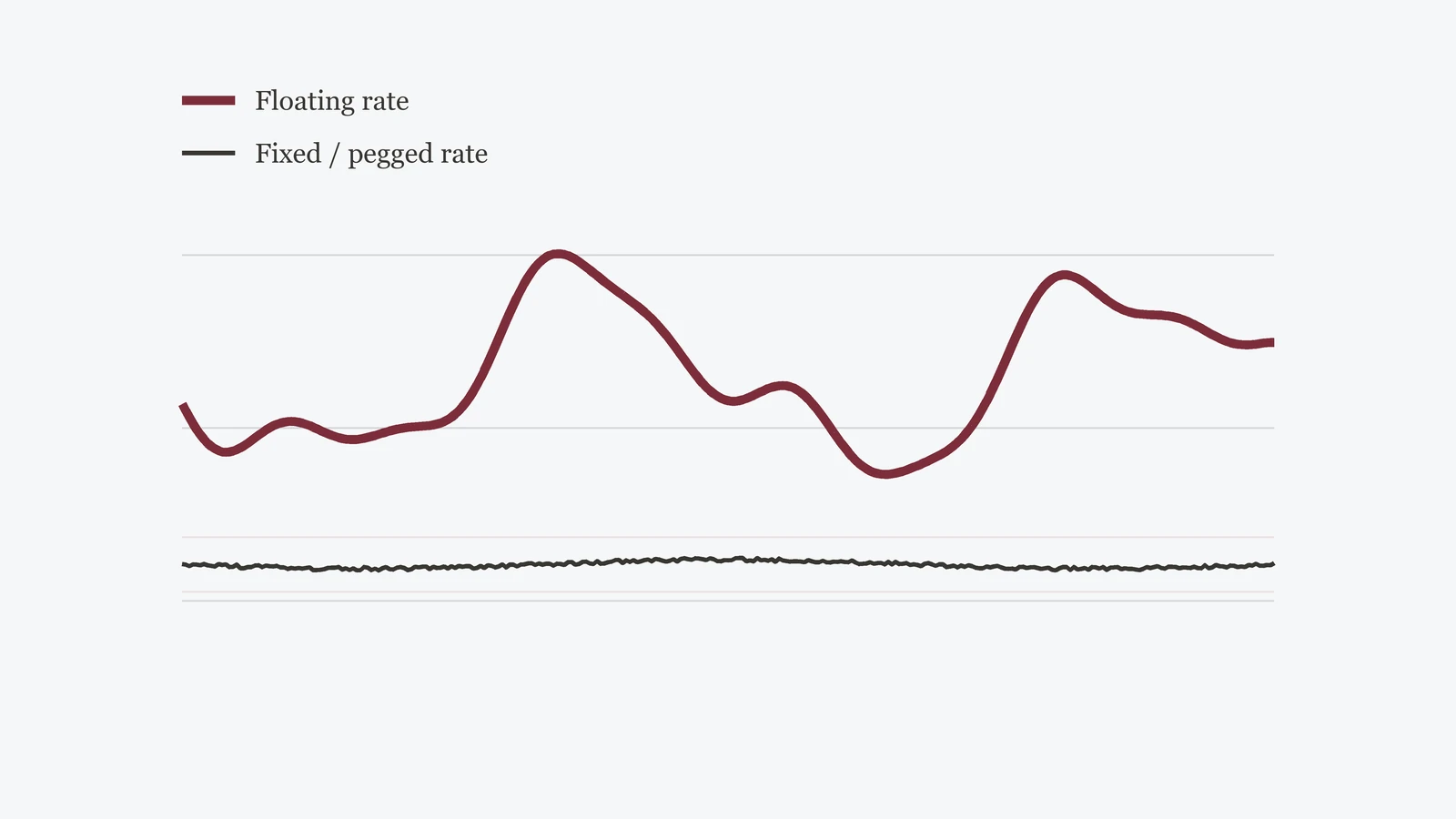

Most of the world’s heavily traded currencies float. A floating rate is simply the price at which people are willing to swap one currency for another right now, and it changes as that willingness changes — second by second, all day. No single authority sets it. Instead it reflects the sum of everyone trading: importers and exporters, travellers, investors, companies and, yes, speculators.

What nudges a floating rate up or down is the ordinary machinery of supply and demand — relative interest rates, inflation, trade flows, growth, and shifts in what people expect next. (Our guide on what moves an exchange rate walks through those forces.) The upshot is a rate that’s honest, in the sense that it reflects live conditions, but restless: it can drift gently for weeks and then jump around a news release. Floating gives a country’s central bank freedom to set interest rates for its own economy rather than spending its energy defending a number — the trade-off is that the currency’s value is out of its direct control.

Fixed rates and how a peg is held

A fixed rate is the opposite choice. The authorities announce a target — often against a major currency such as the US dollar, or against a basket of currencies — and then work to keep the market rate at or near that target. When you see a currency sitting at essentially the same number for a long stretch, you are usually looking at a peg being held.

How is it held? Chiefly with reserves and intervention. If the currency starts to weaken past the target, the central bank sells some of its foreign-exchange reserves to buy its own currency, propping demand up. If it strengthens past target, it does the reverse, selling its own currency and accumulating reserves. Interest-rate policy is often bent to the same job — raising rates to make the currency more attractive and defend the peg, for instance. The key point for a plain-English reader is that a fixed rate is actively maintained. It looks calm on the screen because effort and reserves are being spent, out of sight, to keep it calm. That effort has limits: reserves are finite, and defending a peg the market is pushing hard against can become very expensive.

Floating buys a country policy freedom at the cost of a jumpy currency. A fixed rate buys stability and predictability at the cost of policy freedom — and the ongoing cost of defending the number. Neither is “better” in the abstract; each is a set of trade-offs a country weighs for its own situation.

The managed float in between

Real life is rarely at the extremes. Many currencies run a managed float — sometimes called a “dirty float.” The rate is mostly left to the market, but the central bank steps in occasionally to smooth out disorderly moves or to lean against a swing it considers excessive. It isn’t committed to a specific number the way a peg is; it just reserves the right to intervene now and then.

Think of the three arrangements as a spectrum rather than three boxes. At one end, a pure float the authorities leave entirely alone. At the other, a rigid peg defended come what may. The managed float sits in the middle, and most countries land somewhere along that line rather than at a tidy endpoint. Where a country sits can also shift over time as its circumstances and priorities change.

Types of peg: hard, crawling, band

“Fixed” isn’t one thing either. Pegs come in several forms, differing mainly in how rigidly and how permanently the target is held.

| Type of peg | How it works | Feel |

|---|---|---|

| Hard peg | Rate fixed tightly to another currency, sometimes with a legal or institutional commitment to back it | Very rigid |

| Crawling peg | Target adjusted gradually over time, in small steps, rather than held perfectly still | Slowly moving |

| Band (target zone) | Rate allowed to move freely within an announced range; the bank defends only the edges | Loosely fixed |

A hard peg aims to hold a single rate as firmly as possible. A crawling peg accepts that the target should shift a little over time — often to keep pace with inflation differences — and moves it in small, planned increments. A band, or target zone, gives the rate room to breathe: it can float within an announced range, and the central bank only intervenes when it reaches the top or bottom of that range. These are general descriptions of how the mechanisms work, not a claim about any specific country’s current arrangement — those change, and are set by each country’s own authorities.

What a peg break means for ordinary people

A peg holds until it doesn’t. If a central bank runs low on reserves, or decides the cost of defending a target has grown too high, it may widen the band, move the target, or let the currency float. When a peg is abandoned or breaks, the rate can move sharply — and because it had been held artificially steady, the adjustment when it comes is often large and quick rather than gradual.

For an ordinary person, the mechanics matter more than the headline. If a pegged currency weakens abruptly, imported goods and foreign travel can get more expensive in short order, and savings held in the local currency can lose purchasing power against foreign currencies. That is simply what a lower exchange rate does — the same effect a floating currency has when it falls, just concentrated into a shorter window. None of this is a prediction about any particular currency; it is the general shape of what a peg break involves, so that when it appears in the news the story makes sense.

Understanding the mechanism is useful; acting on a guess about timing is not. No one reliably calls when or whether a peg will move, and framing a currency bet as a sure thing is a classic sign of a bad pitch. This guide explains how the plumbing works — it doesn’t tell you a rate is about to do anything.

Why this matters when you convert or travel

The practical payoff is that the regime tells you roughly what to expect from a rate. If you’re converting into, or travelling to, a country with a floating currency, expect the rate to drift between the day you plan and the day you pay — sometimes barely, sometimes noticeably — so it’s worth checking close to when you act. If the currency is pegged, the headline rate may look reassuringly stable, but two cautions apply: the rate you actually get still includes a margin and fees on top of the official rate, and a peg is a policy that can change rather than a permanent guarantee.

Either way, the regime doesn’t change the basic discipline of getting a fair conversion — comparing against the mid-market rate and watching the fees. It just sets your expectation for how much the underlying number is likely to move while you’re deciding. That expectation is the useful thing to carry away: not a forecast, just a sense of the terrain.

How a peg is actually defended

The word “defend” sounds dramatic, but the mechanism is plumbing. A central bank holds a stock of foreign-exchange reserves — typically dollars, other major currencies, and gold — and uses them to push the market rate back toward its target. When the local currency starts to weaken past the target, the bank steps into the market and buys its own currency, paying for it out of those reserves. That extra demand supports the price. When the currency is instead strengthening past target, the bank does the reverse: it sells its own currency and takes in foreign reserves, which both caps the rate and quietly rebuilds the war chest.

The two directions are not symmetric, and this is the part worth understanding. Defending against a currency that wants to strengthen is comfortable — the bank can print its own currency to sell more or less indefinitely. Defending against a currency that wants to weaken is where the strain lives, because the bank can only buy its own currency for as long as it has reserves to spend. Every day the market pushes the other way, some of the reserve stock is used up. Interest-rate policy usually gets pulled into the same fight: raising rates makes it more rewarding to hold the local currency, easing the pressure, but it also tightens conditions on the domestic economy whether or not that suits it.

“Running out of reserves” is less a single moment than a squeeze. As the stock shrinks, the market can see it shrinking, and the sight of a thinning defence tends to invite more pressure rather than less. At some point the bank faces a plain arithmetic choice: keep spending a finite resource to hold a number, or stop. When it stops — by widening the band, moving the target, or letting the rate go — the adjustment that had been held back tends to arrive all at once. That is the general shape of the mechanism, not a claim about any particular country’s reserves today.

Currency boards and dollarization

Past the ordinary hard peg sit two of the firmest commitments a country can make to a fixed rate. The stricter version of a peg is a currency board: an arrangement in which every unit of local currency in circulation is backed, by rule, with a matching amount of foreign reserves — often close to one-for-one. Because new local currency can only be issued when reserves come in to back it, the board can’t simply print to paper over a defence. That rigidity is the point. It makes the commitment highly credible, which is often exactly what a country adopting one is trying to buy. The cost is that the central bank gives up most of its room to set interest rates or respond to a downturn on its own terms; monetary policy is effectively outsourced to whatever anchor currency the board is tied to.

Dollarization goes one step further and drops the local currency altogether, adopting another country’s money — often, but not always, the US dollar — for everyday use. (The generic term is the point here, not the specific currency; the same logic applies to adopting any external anchor.) There is then no exchange rate to defend, because there is no separate currency to hold a rate against. Stability against the anchor is essentially total. In exchange, the country hands over its monetary controls entirely: it can’t set its own interest rates, can’t adjust its exchange rate to cushion a shock, and can’t act as a lender of last resort in the way an issuer of its own currency can. The pattern across both arrangements is the same trade the whole spectrum is built on, just taken to the limit: the more firmly a country locks in stability, the more of its own policy control it gives away.

Why a country picks one regime over another

Put the arrangements side by side and the choice comes down to a single tension: stability and credibility on one side, the freedom to adjust on the other. A fixed rate or peg offers predictability. Prices and contracts denominated in foreign currency stay steady, cross-border trade is easier to plan, and a firm peg can help anchor expectations about inflation. For an economy that trades heavily, borrows in foreign currency, or is trying to establish credibility after a turbulent stretch, that steadiness can be worth a great deal.

The bill for it is flexibility. A country holding a peg largely gives up an independent interest-rate policy, because rates have to serve the exchange rate first. It also loses the exchange rate itself as a shock absorber: when a floating currency falls, that fall can cushion a blow to exports or a swing in commodity prices more or less automatically, whereas a pegged economy has to absorb the same shock through other, usually more painful, channels. A floating regime keeps both of those tools but accepts a currency that moves on its own schedule and can be volatile when conditions turn.

There is no ranking that holds everywhere. The right regime depends on how open the economy is, how much it borrows abroad, how disciplined its own policy is, and what it most needs to reassure the world about. That is why real countries scatter across the whole spectrum rather than converging on one answer — and why a country can change its mind as its circumstances shift. The useful takeaway isn’t which regime wins; it’s that every regime is a deliberate trade, buying one thing by giving up another.

Questions people ask

What is the simplest difference between a fixed and a floating rate?

A floating rate is set by the market — supply and demand move it continuously. A fixed, or pegged, rate is held at or near a chosen value by a central bank, which buys and sells currency and reserves to keep it there. Floating moves freely; fixed is deliberately held steady until the authority can no longer, or chooses no longer, to hold it.

What is a currency peg?

A currency peg is a policy of tying one currency’s value to another currency (or a basket of them) at a set rate or within a set band. The central bank defends the peg by trading its own currency against foreign-exchange reserves — buying its currency when it weakens, selling it when it strengthens — to keep the rate near target.

Why is my currency pegged to the dollar?

Countries peg to a major currency — often the US dollar — mainly for stability: it can make prices and trade more predictable, anchor expectations about inflation, and simplify pricing for exporters and importers. It is a policy choice with trade-offs, not a fixed law of nature, and the specific reasons differ from country to country.

What happens to ordinary people if a peg breaks?

If a peg is abandoned or breaks, the currency can move sharply, often weakening. Imported goods and foreign travel can become more expensive quickly, and savings held in the local currency can lose purchasing power against foreign currencies. This guide doesn’t predict when or whether that happens — it just explains the mechanism so the news makes sense.

- International Monetary Fund — material on exchange-rate regimes and arrangements: imf.org

- Bank for International Settlements — research on foreign-exchange markets and central-bank intervention: bis.org

- European Central Bank — background on exchange rates and monetary policy: ecb.europa.eu

Last updated 6 July 2026. This guide explains exchange-rate regimes and currency pegs in general terms; it is not investment, tax or legal advice, and it makes no prediction about any currency. Arrangements are set by each country’s own authorities and change over time — check current official sources for any specific country.

Sign up with the code above for up to 20% off trading fees*. Whatever you decide, confirm the live rates, fees and availability on Binance’s own page first — and never share your password, 2FA code or recovery phrase.

*Up to 20% — you’ll see the exact figure on the Binance sign-up page. This is a sponsored referral link: it won’t cost you more, and the site may earn a commission. See our disclosure.