The seven pairs that make up most of the world’s trading Majors, minors and crosses — the dollar pairs, liquidity, and why they move together

If you’re trying to decide which currency pairs are worth understanding first, start here. This guide explains what makes a pair a “major,” how minors and crosses differ, and why a handful of pairs dominate the entire foreign-exchange market. It’s a plain-English reference for anyone making sense of the currency landscape — not a trading method, and it won’t tell you which pair to buy or where any rate is headed.

On this page

- The short answer

- What makes a pair a “major”

- The major pairs, one by one

- Minors and crosses

- Minors and crosses in practice

- Why liquidity matters to you

- Why the majors cost less to trade

- Why some pairs move together

- Why chasing thin “exotic” pairs costs more

- Exotic pairs and why they’re expensive

- How the session changes a pair’s liquidity

- Traps to avoid

- Questions people ask

The short answer

A “major” currency pair is one that involves the US dollar and trades in enormous volume — deep liquidity, in market terms. There are roughly seven of them, and together they account for most of the world’s currency turnover. Pairs that don’t involve the dollar are called crosses; less-traded pairs are minors; and thinly traded pairs involving a smaller economy’s currency are exotics. The practical takeaway is simple: the more a pair trades, the tighter the gap between buy and sell prices, and the less your rate moves against you when you convert. That’s why understanding the majors first is the most useful starting point.

What makes a pair a “major”

Two things, really. First, the pair includes the US dollar (USD) on one side. The dollar sits on one side of the overwhelming majority of global currency trades, so any pair quoting another currency against it inherits huge activity. Second, the other currency is itself a heavily traded one — the euro, the yen, the pound, and a few others. Put a top-tier currency against the dollar and you get the deepest, busiest markets in finance.

“Deep liquidity” is the phrase you’ll hear, and it simply means a lot of buyers and sellers are present at any moment. The Bank for International Settlements measures this turnover every three years in its Triennial Survey, and the same names come up at the top each time. There’s no official committee that stamps a pair “major” — the label just reflects where the volume actually is.

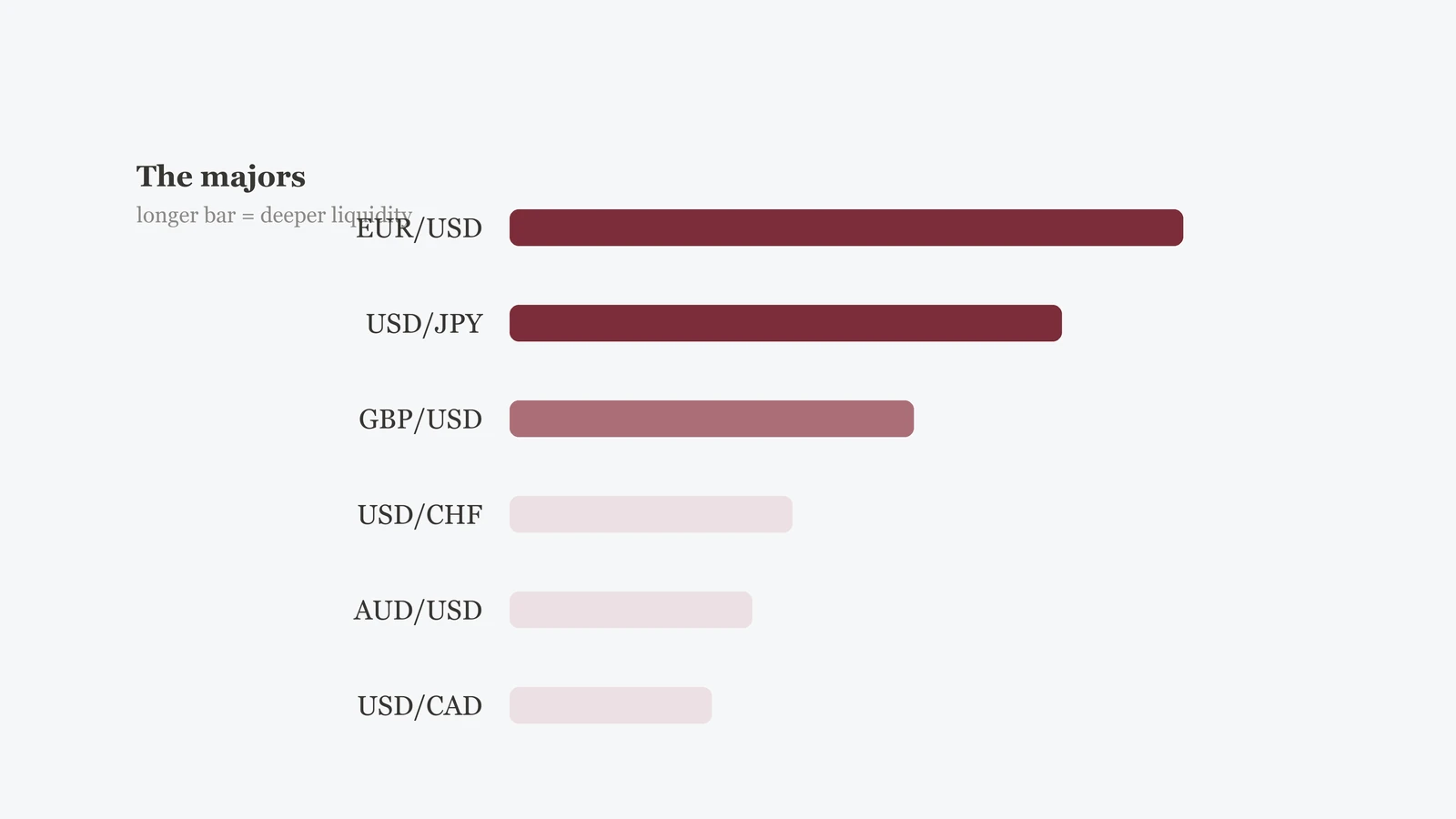

The major pairs, one by one

Here are the pairs almost everyone counts as majors, with the nickname you’ll see traders use and a note on what each is broadly sensitive to. Read the table as a rough map of general tendencies, not a forecast — any currency can move for reasons not listed here.

| Pair | Common nickname | What it’s broadly sensitive to (general, illustrative) |

|---|---|---|

| EUR/USD | “Euro” / “Fiber” | Euro-area vs US interest-rate expectations and growth |

| USD/JPY | “Gopher” | Rate gaps and broad shifts toward or away from safe-haven flows |

| GBP/USD | “Cable” | UK policy, growth and political news vs the dollar |

| USD/CHF | “Swissy” | Safe-haven demand for the Swiss franc; broad risk sentiment |

| AUD/USD | “Aussie” | Commodity demand and global growth sentiment |

| USD/CAD | “Loonie” | Oil prices and the Canada–US economic link |

| NZD/USD | “Kiwi” | Commodity exports and risk appetite |

The sensitivities above are general tendencies that show up over time, not rules and certainly not predictions. A pair can ignore its “usual” driver for long stretches. The reason to learn these names first is that they’re the ones you’ll actually encounter most — in news, in conversion screens, and in any broker or exchange’s quote list.

Minors and crosses

Once you step away from the dollar, the vocabulary changes. A cross is a pair that doesn’t involve USD at all — EUR/GBP or EUR/JPY, for example. Historically you’d convert one currency to dollars and then to the other; a cross quotes the two directly. Minor is a looser term for actively traded pairs outside the top tier — often crosses between major currencies. They still trade in real volume, just less than the headline dollar pairs.

The line between “minor” and “exotic” isn’t fixed, but the spirit is clear. A cross of two major currencies is a minor; a pair that includes a thinly traded currency from a smaller economy is an exotic. The further you go from the majors, the less liquid the market — and liquidity is the thing that quietly determines your cost.

Minors and crosses in practice

Definitions only take you so far. It helps to look at three crosses you’ll actually run into and notice how each behaves next to the dollar pairs it’s built from.

EUR/GBP is the euro against the pound — two of the biggest currencies in Europe, quoted directly. It tends to be the calmest of the three, because both legs are heavily traded and the two economies sit close together. Day to day it often moves in a narrower range than either EUR/USD or GBP/USD on their own, since a piece of news that lifts the euro against the dollar may lift the pound too, leaving the cross roughly where it was. That’s the general pattern, not a promise — a purely UK or purely euro-area event can still push it around.

EUR/JPY pairs the euro with the yen, and it inherits the yen’s tendency to react to shifts in broad risk sentiment. When markets turn nervous and money drifts toward the yen as a safe haven, EUR/JPY often softens; when confidence returns, it tends to firm. It behaves, loosely, like a barometer of how relaxed or anxious markets feel, rather than a bet on Europe versus Japan specifically.

GBP/JPY — nicknamed “the beast” or “the dragon” by some traders — is the one to respect. It combines the pound’s sensitivity to UK news with the yen’s risk-driven swings, so its daily range is typically wider than either EUR/GBP or EUR/JPY. Wider range means larger moves in both directions, which is a way of saying more can go wrong, not that there’s more to gain. Beginners often underestimate how quickly it travels.

Mechanically, a cross is knitted together from its two dollar legs, so its behaviour is a blend of theirs. Understanding the majors first isn’t academic — it’s what lets you read a cross without being surprised by it.

Why liquidity matters to you

This is the part that touches your wallet, even if you never trade. When a pair is deeply liquid, the gap between the buy price and the sell price — the spread — tends to be narrow, because so many participants are competing. A narrow spread means you lose less crossing from one side to the other. When a pair is thin, the spread widens, and you can also get slippage: the price you’re shown shifts before your conversion completes, because there aren’t enough orders nearby to hold it steady.

- Tighter spreads. On busy major pairs, the buy/sell gap is usually small, so converting costs less.

- Less slippage. Deep markets absorb your order without the price jumping away from you.

- Steadier quotes. Prices on liquid pairs tend to update smoothly rather than in sudden lurches.

- Easier comparison. Because majors are quoted everywhere, you can sanity-check one provider’s rate against a neutral reference.

“Liquidity” sounds abstract until you tie it to the spread. The deeper a pair trades, the tighter the buy/sell gap tends to be — and that gap is a cost you pay every single conversion. See bid, ask and the spread for the mechanics.

Why the majors cost less to trade

Follow the chain and the whole thing makes sense. Heavy trading means many buyers and sellers standing ready at once. That crowd competes to offer the best price, which pushes the buy and sell quotes close together. A tight buy/sell gap is a small spread, and a small spread is a small cost every time you cross the pair. Liquidity, in other words, is upstream of your bill.

The table below shows the shape of that relationship, not live prices. Spreads move constantly with the market and vary by provider, so treat these as typical, illustrative ranges rather than quotes — the point is the order of magnitude, not the decimals.

| Pair type | Example | Typical liquidity | Illustrative spread (relative) |

|---|---|---|---|

| Major | EUR/USD | Deepest | Tightest — often a small fraction of a percent |

| Major | USD/JPY | Very deep | Very tight, close behind EUR/USD |

| Minor / cross | EUR/GBP | Solid, below the top dollar pairs | Wider than the majors, still moderate |

| Minor / cross | GBP/JPY | Good, but choppier | Wider again, and less steady |

| Exotic | A smaller-economy currency vs USD | Thin | Widest — can be many times a major’s |

Read down the “liquidity” column and the “spread” column together and they track each other: as one thins out, the other widens. There’s no number here to memorise. What’s worth carrying away is the direction of the link — deeper markets, cheaper crossings — because it holds even as the actual figures drift from one day and one provider to the next.

Why some pairs move together

Currencies aren’t islands, so certain pairs tend to drift in loosely related ways. These are general tendencies observed over time, not predictions — any of them can break down without warning.

The Australian and Canadian dollars are often called commodity currencies, because their economies lean on exporting raw materials. When global demand for commodities is broadly strong, both currencies frequently find support; when it weakens, they often soften together. The New Zealand dollar tends to travel in similar company. None of this is a rule you can trade on — it’s just a tendency worth recognising so the moves don’t look random.

On the other side sit the safe-haven currencies. In nervous markets, money has historically tended to flow toward the US dollar, the Japanese yen and the Swiss franc, which can lift those currencies even when nothing specific changed in their home economies. Again, this is a broad pattern, not a guarantee — safe-haven flows have surprised plenty of people who assumed they were dependable.

Why chasing thin “exotic” pairs costs more

It’s tempting to think the less-watched pairs hold hidden bargains. In practice, the opposite is usually true for your costs. Exotic pairs trade in far smaller volume, so spreads are wider and slippage is more common — you pay more to get in and out, before anything else happens. They can also move sharply on a single piece of news because there are fewer participants to cushion the swing.

- Check how the pair is normally quoted and whether you can even find a neutral mid-rate for it.

- Compare the spread you’re shown against a major pair at the same moment — if it’s far wider, that’s the liquidity cost showing up.

- Consider whether you actually need that pair, or whether routing through a major currency first is cheaper and clearer.

- Treat any “special opportunity” framing around an obscure currency as a reason to slow down, not speed up.

Be very wary of anyone presenting a thin, exotic pair as a “secret opportunity” the majors supposedly hide. Low liquidity means higher costs and bigger surprises, not an edge. Pressure to act fast on an unfamiliar currency — especially alongside promises of easy gains — is a classic setup, not a tip.

Exotic pairs and why they’re expensive

The wide spread on an exotic is the visible cost. Underneath it sits a second one that catches people out: gap risk. In a deep market, prices move in small, near-continuous steps because there’s always an order a little higher and a little lower. In a thin one, the nearest orders can be far apart, so when news hits, the price doesn’t glide — it jumps, skipping the levels in between. You can end up filled well away from the number you last saw, with nothing traded at the prices you expected to pass through.

Two other frictions compound it. Exotic pairs are often tied to a single economy’s politics or one export, so a local headline can move them hard while the majors barely notice. And some carry practical hurdles — local trading holidays, thinner hours, or restrictions on how the currency moves — that a beginner rarely sees coming until a conversion behaves oddly.

So when would you legitimately touch one? Usually because you have a real-world reason rather than a speculative one: you’re paying a supplier, receiving income, or covering costs in that country and simply need the currency. In that case the sensible move is to know you’re paying a liquidity premium, get the all-in figure in writing, and check whether routing through a major currency first works out cheaper. Reaching for an exotic purely because it’s obscure is the version that tends to end badly.

How the trading session changes a pair’s liquidity

Liquidity isn’t a fixed property of a pair — it breathes through the day. A pair is generally at its most liquid, and therefore usually cheapest to trade, when the markets of its own currencies are open. EUR/USD is busiest when Europe and the United States overlap; USD/JPY has more depth while Asian markets are active. Trade a pair in the dead hours between its home sessions and you’re more likely to meet a wider spread and thinner order flow, simply because fewer of the people who normally quote it are at their desks.

This is why the same pair can feel cheap at one hour and clumsy at another, with nothing about the pair itself having changed. For an exotic, the effect is sharper still: outside its local session there may be very little activity at all. The mechanics of who is trading when — the overlaps, the quiet windows, and why they matter — are a topic in their own right; the companion guide on market hours and sessions walks through them. For here, the single idea worth holding is that when you convert can move your cost as much as which pair you pick.

Traps to avoid

A few misunderstandings come up again and again:

- Assuming “major” means “safe.” Majors are liquid, not low-risk. Liquidity affects your cost to transact; it says nothing about which way a rate will move.

- Reading the nicknames as forecasts. “Cable” and “Aussie” are just slang. The sensitivities in the table are broad tendencies, not signals.

- Ignoring liquidity on exotics. A wider spread on a thin pair is a real, recurring cost — not a rounding detail.

- Thinking correlations are guarantees. Commodity and safe-haven patterns describe the past in general terms; they break down regularly.

Questions people ask

How many major pairs are there?

There’s no official count, but most lists name around seven — the dollar against the euro, yen, pound, Swiss franc, Australian dollar, Canadian dollar and New Zealand dollar. The exact membership matters less than the idea: majors are the dollar pairs with the deepest liquidity.

What’s the difference between a cross and a minor?

A cross is any pair without the US dollar. “Minor” is a looser label for actively traded non-top-tier pairs, which are often crosses between major currencies. The terms overlap, and usage varies between providers.

Are major pairs cheaper to convert?

Generally the spread is tighter on liquid majors, so the cost to cross from one side to the other is usually smaller. But the rate you’re offered still varies by provider — always reverse the all-in figure from the mid-market rate.

Does any of this apply to crypto pairs?

The same liquidity logic carries over: heavily traded pairs tend to have tighter spreads than obscure ones. If you’re comparing a crypto exchange, check the live numbers on Binance’s own fee page before you act.

- Bank for International Settlements — Triennial Survey of FX market structure and turnover: bis.org

- European Central Bank — euro foreign-exchange reference rates: ecb.europa.eu

- International Monetary Fund — exchange-rate concepts and data: imf.org

- Federal Reserve — US dollar exchange-rate data and background: federalreserve.gov

Last updated 6 July 2026. This guide is an educational reference on how currency pairs are categorised and why liquidity matters; it is not investment, tax or legal advice, and it is not a trading method. Currency markets change constantly and rules can vary by country — check your local rules and confirm live figures on the provider’s own page.

Sign up with the code above for up to 20% off trading fees*. Whatever you decide, confirm the live rates, fees and availability on Binance’s own page first — and never share your password, 2FA code or recovery phrase.

*Up to 20% — you’ll see the exact figure on the Binance sign-up page. This is a sponsored referral link: it won’t cost you more, and the site may earn a commission. See our disclosure.