How a 2% move can wipe out 100% of your money Leverage and margin in plain terms: what 1:30 really means, and how accounts blow up

If you’ve seen a broker say “trade with 1:30 leverage” and nodded along without quite grasping what it does to your money, this guide is for you. We’ll explain — in plain English — how a small deposit ends up controlling a large position, and why that arrangement is the single biggest reason a tiny price move can erase an entire account. This is an explanation of risk. It is not encouragement to trade, and nothing here is a strategy or a recommendation to open an account.

On this page

- In one breath

- What leverage actually is

- What margin is

- A worked example: how a small move becomes a big loss

- Margin call and stop-out

- Why regulators in some regions cap retail leverage

- The asymmetry — and losing more than you put in

- Why this ties to most retail accounts losing money

- When to stop — red flags

- Where beginners get burned

- Questions people ask

In one breath

Leverage lets you control a large currency position while putting up only a small deposit. It does one thing, and it does it in both directions: it multiplies your gains and your losses by the same factor. That symmetry is the whole story. Because your real exposure is many times your deposit, a price move that looks trivially small — a fraction of a percent, a percent, two percent — lands on your account magnified. With high enough leverage, a 2% move against you can wipe out 100% of the money you put in. Most people who lose money trading currencies lose it here, not to some exotic mistake.

What leverage actually is

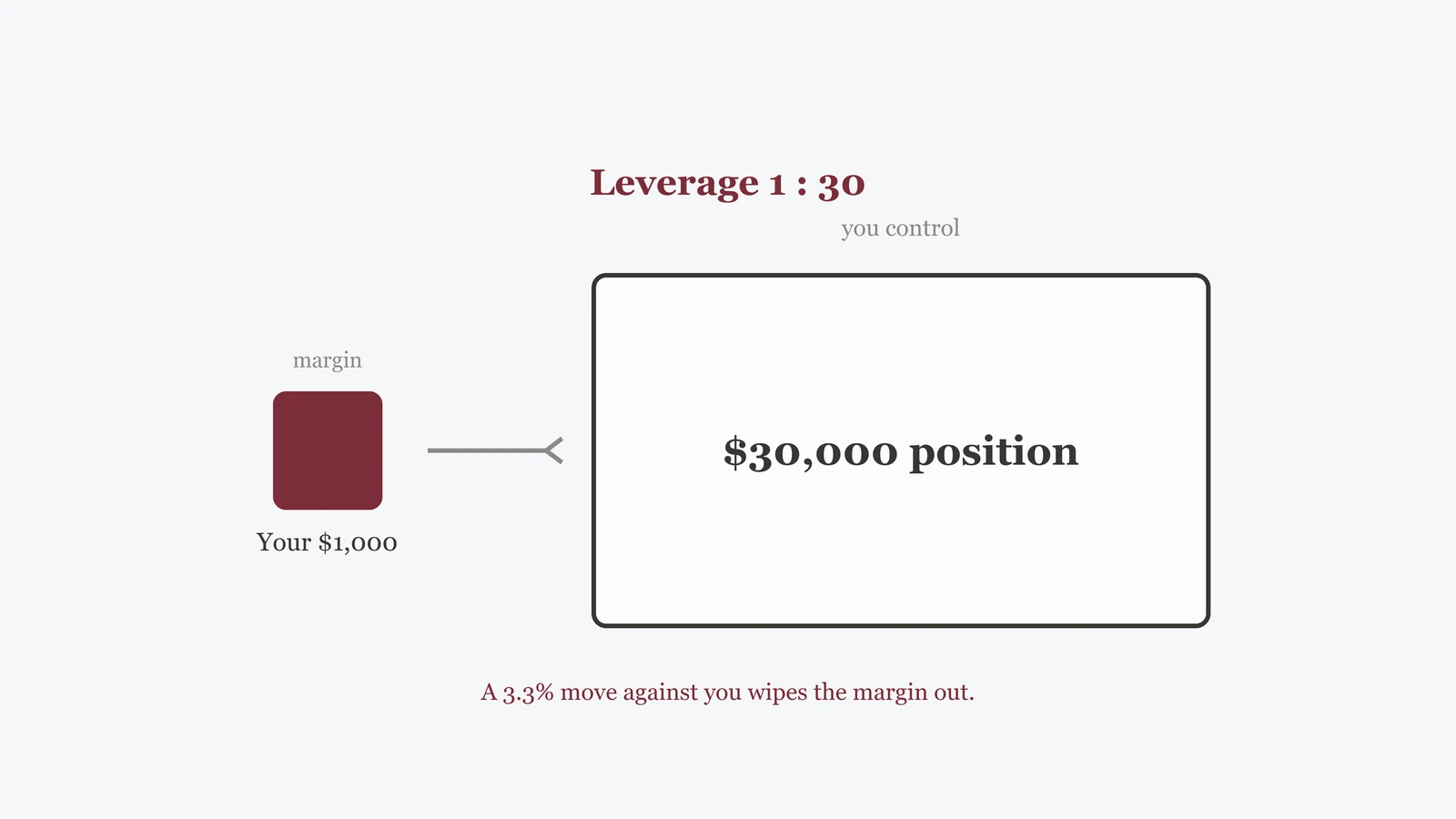

Leverage is borrowing, expressed as a ratio. When a broker offers “1:30,” it means that for every 1 unit of your own money you place as a deposit, you can open a position worth up to 30 units. Put up 1,000 of your currency and you can control a position of 30,000. The position is the thing that moves with the market; your 1,000 is just the slice you’ve committed to back it.

Picture a magnifying glass held over the market’s movements. The currency itself wobbles by small amounts — major pairs often move well under 1% in a day. Leverage is the lens: it doesn’t change how far the currency moves, it changes how large that movement appears on your account. At 1:30, a move is magnified thirty times relative to your deposit. What the lens enlarges, it enlarges regardless of whether the trade is going your way or against it.

This is why “high leverage” is not a feature in the way a faster phone is a feature. It is simply a magnification setting. A bigger number is not better; it is just a stronger lens, and a stronger lens enlarges whatever it is pointed at.

What margin is

Margin is the deposit. It’s the slice of your own money the broker requires you to set aside to open and hold a leveraged position — effectively a good-faith stake against the borrowed exposure. Leverage and margin are two sides of one coin: 1:30 leverage means a margin requirement of about 1/30, or roughly 3.3% of the position’s value. Control 30,000 and you might need to post around 1,000 as margin.

The crucial point is what margin is not. It is not the most you can lose. It is the minimum you must hold for the position to stay open. As the market moves against you, your losses are drawn from that margin, and the cushion shrinks. When it shrinks too far, the broker steps in — which is the next two sections.

Leverage and margin describe the same arrangement from two ends. Higher leverage = smaller margin required = larger position for the same deposit = a smaller price move needed to wipe that deposit out. They rise and fall together.

A worked example: how a small move becomes a big loss

Numbers make this concrete. Suppose you deposit 1,000 as margin and use 1:30 leverage to open a position worth 30,000 in a currency pair. The table below shows what happens to that 1,000 deposit as the rate moves by small percentages against you. These figures are illustrative, not a quote — they ignore spreads, fees and overnight costs, which only make real outcomes worse.

| Move against you (illustrative) | Loss on a 30,000 position | As % of your 1,000 deposit |

|---|---|---|

| 0.5% | 150 | 15% |

| 1% | 300 | 30% |

| 2% | 600 | 60% |

| 3.3% | 1,000 | 100% |

Read the bottom row slowly. A move of roughly 3.3% — the kind of swing a currency can produce around a surprise data release or a central-bank decision — is enough to erase the entire deposit at 1:30. Turn the leverage up and the wipe-out point moves closer: at higher multiples it can take a move of well under 2%. The currency didn’t crash. It barely twitched by the standards of most markets. The magnifying glass did the rest.

Leverage doesn’t make small moves bigger in the market. It makes them bigger on your account — a loss just as readily as a gain.

Margin call and stop-out

Brokers don’t let losses run forever, because the borrowed exposure is partly theirs to protect. Two mechanisms kick in as your deposit erodes. A margin call is the warning: your losses have eaten into the cushion to the point where the broker flags that you need to add funds or reduce the position. A stop-out is the action: if the cushion keeps shrinking past a set threshold, the broker automatically closes your positions to stop the bleed — whether you’re watching or not, and whether or not the rate is about to turn back.

That last part stings the most. A stop-out can close your position at the worst moment, right before a recovery, locking in the loss. You don’t get a vote, and a fast-moving market can blow through the threshold so quickly that the position closes well past it. The protection that stops your account going negative is also the mechanism that can crystallise a loss you’d have ridden out unleveraged.

Why regulators in some regions cap retail leverage

Here is a fact worth sitting with: regulators in some regions limit how much leverage brokers may offer to ordinary retail customers. They didn’t arrive at caps for fun. They did it after watching large shares of retail traders lose money, with high leverage a recurring thread in the wreckage. Where caps exist, the headline retail figure for major currency pairs is often far below the eye-watering ratios advertised elsewhere — a deliberate brake on how fast an account can be destroyed.

The exact limits differ by jurisdiction and change over time, so don’t treat any single number as universal — the rules where you live are what apply to you. But the direction is telling. When public-interest regulators look at retail leverage, their instinct is to restrict it, not expand it. A broker dangling far higher leverage than your local rules permit isn’t offering you a better deal; it may be operating outside the protections built for people in your position. Investor-education and securities bodies publish plain-language material on these risks — see the sources below.

The asymmetry — and losing more than you put in

There’s a brutal asymmetry hiding in the arithmetic. A loss and the recovery needed to undo it are not equal. Lose 50% of your account and you need a 100% gain just to get back to even. Lose 80% and you need to quintuple what’s left. Leverage drives you down that curve fast, and the climb back is far steeper than the fall.

Worse, in some circumstances losses can exceed the deposit altogether. If the market gaps — jumping over price levels with no chance to close in between — a position can blow past your margin before a stop-out fires, leaving a balance below zero. Whether you’re personally on the hook for that shortfall depends entirely on where you are and the protections in force: some jurisdictions require brokers to offer negative-balance protection for retail clients, and others don’t. We’re not going to hard-code a rule, because there isn’t one global answer — check what applies under your local rules and your specific account before assuming you’re shielded.

“The most I can lose is my deposit” is true only where negative-balance protection applies to your account. In a violent, gapping market without that protection, the loss can run past what you put in. Confirm before you ever rely on a floor.

Why this ties to most retail accounts losing money

Brokers in regulated regions are often required to publish the share of retail accounts that lose money. The figures are sobering — a large majority, consistently. There’s no single villain, but leverage is woven through every part of the explanation. It shrinks the move needed to trigger a loss. It speeds up stop-outs. It punishes small mistakes that would be survivable unleveraged. And it interacts with costs — spreads and overnight charges are levied on the full position size, not your deposit, so the magnifying glass quietly enlarges your running expenses too.

None of this means a particular outcome is certain for any one person. It means the structure is tilted, and high leverage steepens the tilt. If you take one idea away, make it this: the number a broker advertises as a benefit is the same number a regulator treats as a hazard.

When to stop — red flags

Close the tab and walk away if you encounter any of these:

- Extreme leverage as a selling point. Offers of leverage far above what your local rules allow for retail clients aren’t generosity — they signal you may be outside the protections meant for you.

- “Guaranteed” anything. No one can guarantee a profit, a return, or that you won’t lose. Anyone who claims otherwise is misleading you.

- Pressure to decide now. Countdown timers, “limited spots,” a coach urging you to fund immediately — urgency is a tactic, not a reason.

- Deposit more to unlock something. Being pushed to add funds — for a “tier,” a bonus, or to release money supposedly already yours — is a classic warning sign, not a perk.

Where beginners get burned

The errors that hurt people most are predictable:

- Reading leverage as opportunity, not exposure. “1:30” is not 30 times the chance to win. It is 30 times the magnification of whatever happens — loss included.

- Confusing margin with maximum loss. Margin is the minimum to stay open, not a cap on what you can lose. Without negative-balance protection, losses can run further.

- Sizing against the deposit instead of the position. What moves with the market is the full position. A “small” 1,000 deposit can be backing a 30,000 exposure you’re mentally ignoring.

- Assuming a stop-out will save you at a tidy price. In fast or gapping markets, positions can close well past the threshold, deepening the loss.

- Maxing out the leverage on offer. Being allowed 1:30 is not a reason to use 1:30. The higher the multiple, the smaller the move that ends you.

If you ever do trade, how to keep the risk small

To be clear, this is not a nudge to start — the safest amount of leverage for most people is none. But if you are going to be in this arena, these steps keep the magnification dialled down rather than up. They reduce risk; they do not remove it.

- Use the lowest leverage you can, not the highest you’re offered. Treat the advertised maximum as a hazard ceiling, not a target.

- Size by the position, never the deposit. Work out the full exposure you’re controlling and ask what a realistic adverse move does to your account.

- Risk only money you can lose entirely. Never funds you need for rent, food, debt or anything that matters. Assume it could go to zero.

- Confirm whether negative-balance protection applies to your account. Don’t assume your deposit is the floor — verify it under your local rules.

- Decide your exit before you enter. Know in advance the loss at which you’ll close, and don’t move it once the trade is live.

- Check the broker is authorised where you live. Use only a provider regulated under your own jurisdiction’s rules, and read what those rules actually protect.

Questions people ask

Does higher leverage mean higher potential profit?

It means higher magnification, full stop. Gains and losses are scaled by the same multiple, so “more profit potential” always comes bolted to “more loss potential.” There is no version where only the upside grows.

Can I really lose more than I deposit?

In some circumstances, yes — if the market gaps past your margin before a stop-out fires and your account has no negative-balance protection. Whether you’re liable for the shortfall depends on your jurisdiction and account, so check rather than assume.

Why do brokers offer such high leverage if it’s so risky?

Because the full position size — not your deposit — drives their spreads and fees, and larger positions mean more activity. That’s also why regulators in some regions cap retail leverage: the incentives don’t naturally point toward restraint.

Is the leverage in crypto the same idea?

The mechanics are the same: a small deposit controls a larger position, and the magnification applies to gains and losses alike. If anything, leverage on crypto can be marketed at extreme levels and the assets themselves are often more volatile — see FX vs the crypto market.

- European Securities and Markets Authority — measures on retail leverage and risk: esma.europa.eu

- U.S. SEC investor education — leverage, margin and trading risk: investor.gov

- U.S. Securities and Exchange Commission — rules and investor protection: sec.gov

- Bank for International Settlements — structure of the FX market: bis.org

Last updated 6 July 2026. This guide explains how leverage and margin work and the risks they carry; it is not investment, tax or legal advice, and it is not a recommendation to trade. Leverage limits, negative-balance protection and broker rules differ by country and change over time — the rules that apply to you are your local ones, so confirm them before acting.

Nothing here is a nudge to start — leverage is exactly how small accounts get wiped out. But if you’ve weighed it up and you’re opening a Binance account regardless, the code above takes up to 20% off your trading fees*, at no extra cost. Start small, size every position for the loss you can survive, and never share your password, 2FA code or recovery phrase.

*Up to 20% — you’ll see the exact figure on the Binance sign-up page. This is a sponsored referral link: it won’t cost you more, and the site may earn a commission. See our disclosure.